Checking in on Senegal

hidden debt, total return swaps, and political upheaval in Dakar

For those who haven’t been following (most of us, probably) Senegal is in quite a bind. I don’t follow sovereign debt religiously, but I happened to be in Dakar1 on some track two diplomacy business when I heard official sector observers describe a nation on the verge of crisis. Here’s what I’ve learned.

Background: TL;DR on Senegal’s debt situation

Senegal remains one of the wealthiest countries in the Economic Community of West African States (ECOWAS), and a leader in stable governance, growth, and development in Francophone West Africa. Today, though, it faces a sovereign debt crisis that has been growing for two years. Like many Sub-Saharan African nations, Senegal has had a long history of external borrowing—that is, sovereign debt held by foreigners. Unlike many of its continental counterparts, Senegal has enjoyed broad access to international capital markets and has engaged widely in the regional West African Economic and Monetary Union (WAEMU) debt markets.

The long and short of the current situation is that the previous administration hid a considerable amount of sovereign debt from the public and, incredibly, from the IMF. The current administration called them out on this, but uncovered that the hidden debt was actually quite large (debt-to-GDP of 75% before to ~130% after). The IMF then suspended disbursements from its facility and Senegal was effectively shut out of international bond markets and pushed to source more financing from domestic and WAEMU markets in addition to borrowing from some banks at increasingly strict (including secured) terms. Meanwhile, a “maturity wall” looms, as large groups of coupon payments come due in 2026–2028. Senegal has thus far managed through the crisis by relying on domestic fiscal reforms and leaning more heavily on domestic and regional securities markets. Yet the current situation does not appear sustainable, and pressure is mounting on the government to take larger steps.

Timeline

A timeline is always nifty (2024–today):

Sep. 26, 2024: PM Sonko2 accuses former Sall government of lying to the public after an internal audit report finds considerably larger public debt stock than was previously reported.

Oct. 4, 2024: Moody’s downgrades Senegal’s foreign-currency ratings from B1 to Ba3 and places the ratings on a review for downgrade, citing the hidden debt episode and fiscal pressures.

Oct. 29, 2024: Senegal confirms that the IMF has frozen its USD 1.8 billion program after revelations of accounting scandal.

Feb. 12, 2025: Senegal’s Court of Auditors publishes its official audit report, revealing government debt significantly understated by previous administration.

Feb. 28, 2025: S&P Ratings lowers Senegal’s foreign- and local-currency ratings from B+ to B with a negative outlook, citing the newly revealed debt burden.

March 24–26, 2025: IMF indicates that it will not engage in negotiations for a new program until Senegal has addressed data misreporting and calls for tax and subsidy reforms in light of the audit report debt findings.

May, 2025: Senegal borrows EUR 350 million from the African Finance Corporation via a total return swap, a type of fixed-income derivative; the borrowing is not publicly disclosed at the time.

June, 2025: Senegal borrows EUR 300 million from First Abu Dhabi Bank via a total return swap, a type of fixed-income derivative; the borrowing was not publicly disclosed at the time.

July 14, 2025: S&P Ratings lowers Senegal’s foreign currency credit rating for the second time in five months, from B to B-, its lowest ever S&P rating, citing the nation’s budgetary constraints and debt.

Aug. 1, 2025: PM Sonko announces an economic recovery plan in which 90% of funding will be sourced domestically, avoiding external debt.

Sep. 17, 2025: Government source reports to Reuters that Senegal plans to raise USD 180 million in a domestic sukuk and has plans for an international sukuk issuance in 2026.

Oct. 3, 2025: IMF Managing Director Georgieva says that Senegalese authorities have shown an “admirable commitment to transparency” and that she welcomes Senegal’s request for a new IMF program.

Oct. 13, 2025: Senegal releases its Medium-Term Debt Management Strategy for 2026–2028, acknowledging that the peak repayment period for Senegal in the medium-term would be between 2025–2028, and identifying the local debt market as a source of financing, particularly in the context of the suspended IMF program.

Nov. 6, 2025: IMF team visit to Senegal concludes without a deal, with the IMF issuing a positive statement about “laying the foundation for a new IMF-supported program,” while underlining that further steps are needed on reforms to debt-management and the budget. PM Sonko later indicated that during this visit, the IMF urged Senegal to engage in a debt restructuring.

Nov. 8, 2025: PM Sonko says that despite IMF pressure, a restructuring would be a “disgrace.”

Nov. 11, 2025: PM Sonko says, “Senegal is a proud nation. We will not be treated like a failed state. Mobilizing tax revenue is better than accepting a debt restructuring.”

Nov. 13, 2025: Senegalese finance ministry says it’s committed to IMF dialogue and will honor its debt obligations.

Nov. 14, 2025: S&P Ratings lowers Senegal’s foreign currency debt to ‘CCC+’ citing “precarious” debt position, and places Senegal on a credit watch (signaling a potential future downgrade).

March 17, 2026: S&P Ratings downgrades Senegal’s local currency debt to ‘CCC+/C’ with a negative outlook, citing heightened debt sustainability risks absent an IMF program and growing budgetary needs.

March 23, 2026: The Financial Times breaks article that Senegal had in 2025 borrowed EUR 650 million via opaque derivatives in order to avoid default; the story was the first to publicly disclose this borrowing.

April 15, 2026: Economy Minister Sarr says that Q1 2026 figures from the regional debt market have been supportive of Senegal’s solid macroeconomic fundamentals and should provide optimism for Senegal’s financing resources and the likelihood that Dakar would reach an agreement with the IMF.

May 6, 2026: Senegalese WAEMU-market 3-year bonds auctions for 8.07%, compared to the 5-year yield at 7.73%, interpreted by some observers as a classic yield-curve inversion signaling concern about Dakar’s looming maturity wall.

May 23, 2026: President Faye fires PM Sonko, for reasons that some media outlets suggested was driven by long-simmering disputes over economic policy, not least the debt crisis. The Faye-Sonko coalition had long been considered strongly unified, almost one-in-the-same, after Sonko threw his political capital behind Faye when he was unable to run for president himself.

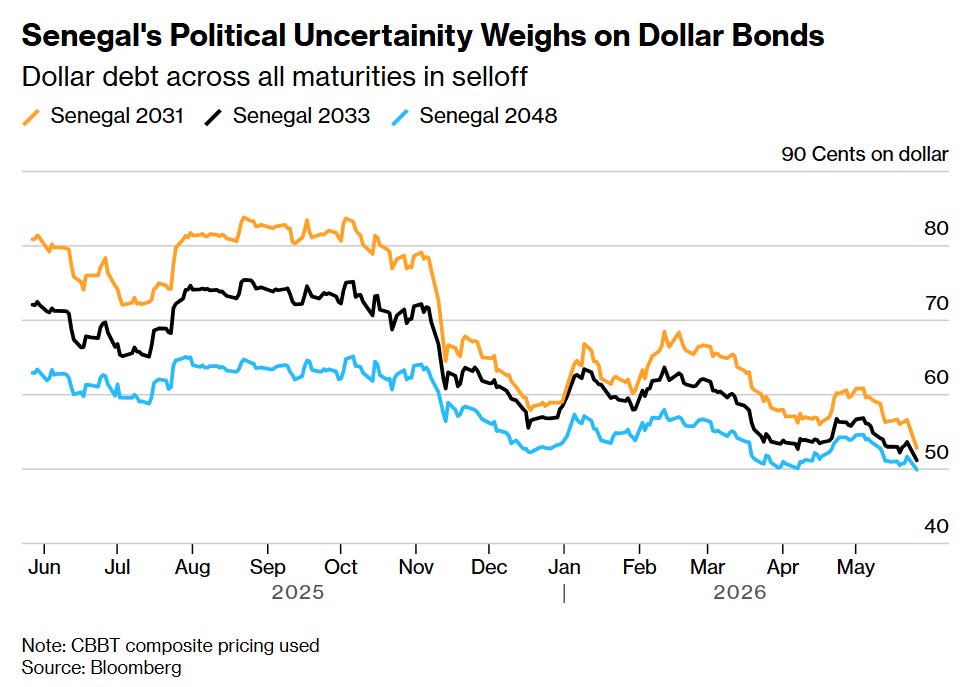

May 26, 2026: Senegal’s dollar bonds fall as investors digest news of the political turmoil; the nation’s 2031 dollar bond falls to trade at 53 cents on the dollar.

Senegalese Dollar Bonds (via Bloomberg):

Year-End 2025 Macro Situation

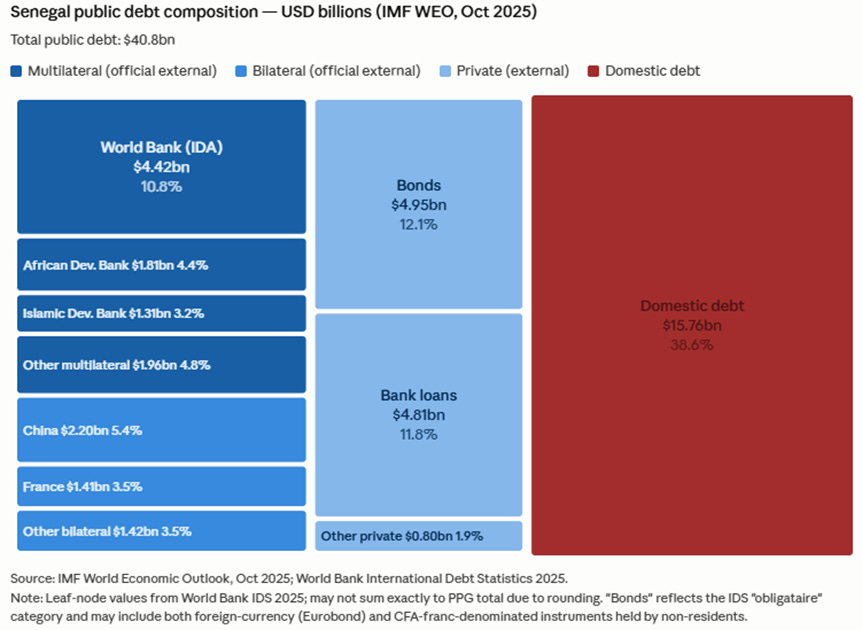

Senegal’s debt stock is very large. Among low- and middle-income countries, Senegal has the second highest debt-to-GDP ratio, only lagging war-torn Sudan. According to FDL, of the 36 episodes in which a developing country has maintained a debt-to-GDP ratio over 100% for several years, only a single one resolved without a default or debt restructuring.3 For reference, the IMF in its Low Income Country Debt Sustainability Framework (LIC DSF) considers a present value of external debt to GDP ratio of 55% as the upper limit of sustainable; by FDL estimates, Senegal’s in 2024 was 73%. Senegal’s debt stock is also largely external, with over 61% of debt held by foreigners at year-end 2024. Here’s a picture of the 2025 debt stock:

There is some good news about Senegal’s debt stock. First, its interest costs are relatively low, estimated at around 23% of revenues, compared to interest costs as high as 90% of government revenues for countries such as Egypt, Kenya, and Pakistan (although that figure has grown considerably by now). Due to a large share of concessional financing (59% of external debt is concessional or semi-concessional), Senegal has an effective interest rate of only 4.5% (although it could well rise to 5.5–6.0% in the medium term). Second, thanks to the CFA-euro peg and the large WAEMU regional market, Senegal has limited foreign exchange risk in its borrowing and benefits from reduced inflation risks. Third, while Senegal does face an acute near-term “maturity wall” in 2026–2028, the redemption schedule after 2028 begins to decline considerably, implying that there is space to refinance the “maturity wall” into the future and smooth redemptions while maintaining a sustainable repayment load.

Gambling for Resurrection: Total Return Swap Deals

After uncovering the previous administration’s hidden debt, Senegal furtively borrowed USD 1.3 billion via seven different derivative products that were not considered a formal part of the nation’s debt. Moreover, this debt is senior to existing bondholders. Dakar used a product known as total return swaps to obtain the loans.

What are total return swaps?

In short, they are what they sound like: I own the S&P; you own the DAX; I agree to pay you the S&P returns; you agree to pay me the DAX returns. In practice, it becomes a little more complicated with fixed-income products, because you need to account for two parts of value: the coupons and the market-to-market value of the bonds. In practice, you might offset them in a lump-sum cash payment (i.e., maybe the coupon I’m to receive is 3% but the value of the bond falls 3% in the same period, you might just net that and pay me $0 of cash).

Dakar’s total return swaps (TRS)

For starters, we still don’t know all the details of the transactions. But I’ll try to outline here the contours of the structures generally, based on publicly available reporting and information from someone familiar with the deals who has seen some of the term sheets. An important caveat, though: Senegal does not appear to have used a common term sheet or terminology across its different deals; they are all bespoke.

Illustrative Example: African Finance Corporation (AFC)

Senegal issues new 2028 6.3% EUR 500 million Eurobond and provides it as collateral and reference asset for the TRS, taking a 30% haircut, so borrowing against (swapping against) EUR 350 million.

Senegal and the AFC enter into the swap for a nominal amount of EUR 350 million: instead of paying its coupon rate, Dakar receives the coupon rate on its Eurobonds (in this case, 6.3%); likewise, the AFC receives (instead of pays) a floating rate of 6-month Euribor + 3.5% (if Senegal’s rating is B3 or above, but it rises if Senegal faces ratings downgrades). If 6-month Euribor has been floating around 2.5%, that leaves the floating rate somewhere around 6%. So, with no valuation adjustments, this is an attractive setup for Dakar: it’s paying something like 6% and receiving something like 6.3%, so potentially even making some money on the TRS interest payments. Note that AFC is getting seniority in this deal, even above existing bondholders (and is also betting that TRSs will be treated as domestic debt, and thus left out of any restructuring . . . they hope).

But it’s not just interest payments. At the first settlement date (less frequent than monthly, as it has been for some of Senegal’s other TRS deals), the parties also need to net the valuation gains (losses). Since the bonds are initially valued at par, the chances of any significant upside appreciation in bond prices is limited, but they can fall all the way to zero. So, assuming the bond prices are falling in value, that mark-to-market top-up also gets paid. Depending on the terms, Senegal may also have to provide more collateral in addition to paying the valuation change (unknown in the case of the AFC deal). (Note also that the haircut on the initially issued bond drags the weighted-average cost of the borrowing up, since Senegal is still paying the coupon on the EUR 150 million of the Eurobond that isn’t in the swap.)

This is a leveraged play on Senegal’s own sovereign debt: if the bonds do well or even appreciate, Senegal is borrowing majorly on the cheap, and maybe even making money, but if the bonds decline, Senegal is doubly penalized. Not only will it have to pay the valuation shortfall (the M2M loss), but if its ratings decline, the floating rate it pays also gets ratcheted up. It’s a highly procyclical move.

Clever financial engineering or risky gamble?

Total return swaps such as these have two advantages. First, if the sovereign bonds issued as collateral (and reference asset) hold their value, the swap structure can provide cheap financing. As we’ve seen, this setup (in the best states of the world, at least) allows Senegal to obtain cheaper financing than it could by issuing a Eurobond directly (and note that, in Senegal’s case specifically, since the CFA is pegged to the euro, there’s essentially no risk in the currency mismatch here, making the structure even more attractive). Senegalese Finance Minister Diba said that the deals costed 7%, relative to 11–12% rates on international markets (at USD 1.3 billion, this rate differential would represent up to USD 65 million in savings). For this reason, total return swaps are increasingly popular among debt-laden countries, particularly in Africa, with for example, Nigeria entering into a similar swap with the same First Abu Dhabi Bank just weeks ago. Second, since the structures are technically derivatives, not traditional loans, they can be excluded from debt statistics, thereby keeping such synthetic borrowing confidential. In the example case of the deal with AFC, the AFC even got bespoke enhanced confidentiality clauses into the deal.

Such structures can be costly. If the collateral (in this case, Senegal’s own newly issued sovereign bonds) fall in value, the borrower can be hit with expensive margin calls, requests for further collateral. Just last year, Angola experienced a USD 200 million margin call on its own sovereign debt total return swap deal with JP Morgan. Moreover, since the swap is a total return swap, not merely an interest rate swap, each payment includes two components: the netted interest rate and the valuation change. So, if the market value of Senegal’s newly issued sovereign bonds fall, then it has to pay more in the swap payment.

Total return swaps can be controversial. In Senegal’s case, not only were the structures not disclosed, but they also granted seniority to the swap counterparties over existing bondholders, essentially subordinating other investors without their knowledge. In at least one of Senegal’s deals (with First Abu Dhabi Bank), the risks are even higher than they first appear, because the bank can require immediate repayment if Senegal’s credit falls below a specified credit-rating threshold. At least some of Senegal’s swap deals appear to include other punitive terms, such as the lender’s ability to mark Senegal’s bonds to zero in the event of default. The primary point of controversy has been the lack of transparency about the swap arrangements. While originally (at the time of initiating the swaps) Senegal did not publicly disclose them, Dakar later disclosed that it had borrowed USD 1.3 billion via seven different swap transactions in 2025 after the Financial Times ran an article uncovering EUR 650 million via two swap deals.

Senegal’s Finance Minister Cheikh Diba has said that the deals resulted in up to 500 basis points of cost savings for the nation; mobilized foreign capital “in a way that strengthened [] liquidity and reassured investors”; and that the swaps were disclosed to key stakeholders, including the IMF. In Dakar’s defense, I wouldn’t probably want to publicly borrow either after the disclosure of the hidden debt; some discretion here probably made sense. Nonetheless, resorting to borrowing via complex derivatives in order to keep up with debt service costs is kind of a cry for help.

Political Shakeup: Does it change the calculus?

What to make of the Sonko dismissal?

In a nutshell, the theory is basically that Sonko had long been more militant in his opposition to restructuring (which he views as fundamentally incompatible with his view of economic sovereignty), and that Faye is more flexible on restructuring. The idea is that the departure of Sonko at Faye’s direction means that a restructuring is more likely. Mr. Sonko is the founder and head of the Pastef party (of which Mr. Faye is a member), and is viewed as more populist than Mr. Faye. That narrative seems consistent with the bond market’s reaction, which priced in a 15% haircut restructuring and a five-year maturity extension after the news of Mr. Sonko’s dismissal.

Notably, it is not only Mr. Sonko who is gone; as head of the party, he has also suspended the party’s participation in the newly created Government (i.e., is providing no ministers). (In reality, some backbencher Pastef members are in fact on the list of the new Government, but the heavyweights appear to be staying on the sidelines.) Mr. Sonko remains the head of Pastef and remains opposed to restructuring; he therefore remains a key figure.

The government shakeup matters materially because Dakar plans to reengage the IMF and hopes to reach an agreement on major points by the end of the month. Cleaning house is a way for Mr. Faye to change Dakar’s negotiating posture with the Fund.

Who is Sonko’s successor?

Ahmadou Al Aminou Mohamed Lô is the new PM, and he is a consummate technocrat, a former Secretary General of the Central Bank of West African States (BCEAO) with considerable experience in bank and financial markets regulation. He is known to be a staunch defender of the CFA Franc. He is so much a figure of the technocratic bureaucracy that the government press release announcing the replacement literally says, “a product of the technocracy, he is a specialist in macroeconomics, banking regulation, financial markets. . . .”

The choice of Mr. Lô sends a clear message: Senegal is serious about fixing its external position, and has, for now, rejected the populist path forward (read: is more open to a restructuring). Again, in the government press release, it states that Mr. Lô, “reassured the local private sector, technical and financial partners, and foreign investors” and emphasizes his experience at the BCEAO with Senegal’s Eurobond issuances and relationships with the ratings houses.

Crystal Ball?

Look, first of all, I am not a sovereign debt expert. Also this is definitely not financial advice. But it seems like the bonds have further to fall before this whole thing gets worked out.

On first principles, a country has a debt crisis when there is more debt than there is income to pay back that debt. At first, the government will try to retrench and pull off austerity, but this rarely works, because it’s growth-negative. Pulling back on services and investment just as the economy faces macro headwinds is usually counterproductive. Eventually, the country is left with two choices: default/restructure, or monetize the debt. Senegal does not have an independent central bank, so option two is off the table. That basically leaves us with successful austerity or default/restructuring. History tells us that the latter is more likely.

Of course, the bond prices could already have a restructuring priced in. Last I checked, they were trading in the mid-50s (50 cents on the dollar I mean). I don’t have a scientific debt sustainability analysis for you, but a systematic naïve approach. We know from academic research (Sovereign Haircuts: 200 Years of Creditor Losses) that, considering 200 years of data and 327 sovereign restructurings, the average haircut hovers around 45%. That probably sets a floor since, per the paper, haircuts are higher when debt stocks are high (Senegal’s is huge); and haircuts are higher for low-income sovereigns (Senegal isn’t the lowest-income in Africa by a margin, but the dataset includes high-income countries like Spain that pull the average up). Per the paper (p. 22), from 1815–2023, the average NPV haircut for restructurings in countries with a debt-to-GDP ratio above 72% is roughly 50%. Further, per the paper (p. 24), lower-middle-income countries (of which Senegal is a member) have a mean haircut of around 40% (but with wide variation, ranging up to 80%).

We could use the regression model the paper provides (p. 31), make some assumptions, and get an (imprecise) estimate of expected haircut. If you assume Senegal is the 19th percentile of global income; has a debt-to-GDP ratio of 130%; will have a default duration of six months (probably conservative?); and has a GDP contraction of 6% (probably conservative?), you get a predicted haircut of around 67%. If that’s off by +/– 10%, that gives us a range of 57–77%. Let’s be conservative and say 60%. Look, the R-squared of the model is 0.57—I wouldn’t hang my hat on this thing. But, naïvely, you might expect bond prices to bottom around 40 cents on the dollar.

We’re still early in the restructuring timetable. We’ve got a new PM, and negotiations with the IMF are set to continue on June 8. This is before any real discussion of the TRS, and seems like the first time we have a government in Dakar that is truly open to good-faith negotiations on a restructuring.

Bon courage, Dakar!

I wish I’d had even more time there, definitely recommend.

Importantly, Senegal is a semi-presidential republic, similar to France. This matters for the ensuing drama.

And even that case is dubious, since Antigua—the sole survivor—did end up restructuring after the 2008 financial crisis.