Dispatch No. 6

Some relevant research and analysis

A User’s Guide to Reducing the Federal Reserve’s Balance Sheet. Alyssa G. Anderson, Alessandro Barbarino, Anthony M. Diercks, and Stephen Miran. Federal Reserve Board.

The Fed’s balance sheet used to be c. 6% of GDP; at its peak, it has reached 36%. Some folks are very worried about this; others are not. To be sure, this article isn’t an endorsement of shrinking the Fed’s balance sheet to any particular level. But this is a very helpful framing of what has become a charged (well, as charged as central banking can get, which isn’t very) topic: should the Fed shrink its balance sheet? If so, how? This is something Governor Miran talks about frequently (here’s a recent speech in which he cites this very article).

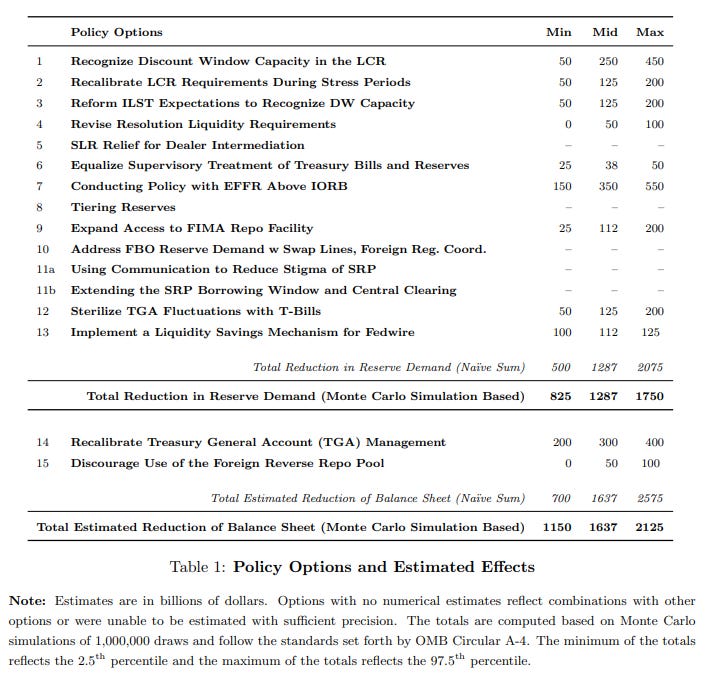

If you stipulate that you’d like to reduce reserves, without even potentially shifting to a scarce-reserves operating framework, then this paper lays out some ways to do that. Here’s a nifty table from the paper:

An aspect that this paper concentrates on—and is completely correct about—is that calibrating the size of the Fed’s balance sheet is not merely a supply question, but also a demand question. Say the authors of the paper on the repo volatility that arose from extended QT:

We cannot conclude from repo volatility alone that the Fed’s balance sheet was unable to be reduced further. If precautionary demand for reserves were lower, it would allow less constrained banks to neutralize shocks by lending into the repo market, which would lower the level of the balance sheet at which repo volatility manifested.

That’s totally right, and something that folks in the financial stability space have been talking about for some time (i.e., if we credit banks’ LCR with discount window access, they may do less precautionary “hoarding,” which would be better for everyone). Here, the authors extend that to the monetary policy framework, which is a helpful and clear connection. There are some interesting proposals, such as operating with the Effective Federal Funds Rate slightly above the Interest on Reserve Balances rate, which would also have the effect of ridding the system of an arbitrage performed by the US branches of foreign banks.

The paper is worth reading in its entirety, but the upshot is basically this line: “Modern monetary policy implementation is defined by the boundaries between scarce, ample and abundant reserves. Those boundaries can be shifted down by modifying the policy landscape, reducing demand for reserves.” Implicit (and explicit in the paper) in that “landscape” is regulatory—often deregulatory—changes. Some of the proposals, such as shifting (at least a sizable chunk of) the Treasury’s cash management from the New York Fed to commercial banks, seem unlikely to gain traction. On the whole, though, these authors have clearly laid out the channels through which shrinkage, even while avoiding a return to a wholesale scarce-reserves framework, could take place.

Seniority, Senegal & Sovereign Creditor Violence. Max Hess. Conflict & Credit.

Some personal bias here, I am a sovereign debt novice (but eager learner/fan) and just happen to have been in Senegal two weeks ago in a meeting with some Western government folks in which I heard all about Senegal’s impending sovereign debt gloom, so this struck me as particularly noteworthy. Some other personal bias, I am a big fan of Max’s work, and if you’re not subscribed to his Substack, you should be:

This article gives color to some “intrepid” reporting (agreed) from the FT about Senegal’s position, which is best described as precarious. Some context: the former administration in Senegal—Macky Sall’s—was found to have hidden considerable amounts of sovereign debt, so much so that the current “auditor government” of Bassirou Diomaye Faye has uncovered debt-to-GDP to be closer to 130% than the roughly 75% reported by Sall’s government. So, bad. But it’s actually worse, because after discovering the hidden debt, Senegal borrowed more. Worse still, the borrowed debt was, in technical terms, crazy. Senegal borrowed via Total Return Swaps (TRS), derivatives that are basically levered positions on Senegal’s own credit. Worse still, these claims are senior to existing bondholders.

Max’s piece is worth a read in full, but I’ll just add from my visit that it felt like a crisis not yet coming to a head. Government folks were certainly aware, but it didn’t feature prominently in many discussions (only one or two), and the main economic complaint seemed to be cost of living. But, like all crises, presumably this will be very slow until it’s very fast. Over to you, IMF.

Stablecoin Flows and Spillovers to FX Markets. Iñaki Aldasoro, Paula Beltrán and Federico Grinberg. BIS and IMF.

As we’ve discussed on this site, the stablecoin-offshore dollar-FX nexus is huge and, in my opinion, probably the most underappreciated angle of stablecoin proliferation. Stablecoins are not just not limited to the US—they’re mostly used and circulated outside of the US.

The authors of this paper, one from the BIS and two from the IMF, show, in a nutshell:

that there are deviations of funding costs in obtaining dollars offshore via stablecoins versus traditional methods (swaps), which are correlated with stablecoin flows and local FX depreciation;

that the global supply of stablecoin liquidity is segmented (in an arbitrage sense), which allows for the deviations;

that a “one percent exogenous increase in net stablecoin inflows raises parity deviations by approximately 40 basis points (bp), depreciates the local currency by 5 bp, and widens the short-term dollar 1 premium by 5-10 bp”;

frictions across markets are the main cause of these deviations.

As they put it:

Our findings demonstrate that stablecoin markets are already linked to traditional finance, with spillovers that affect currency stability and funding conditions. This has direct implications for policymakers concerned with monetary policy autonomy and financial stability, particularly in emerging markets where these effects are most pronounced.

Key to the story is this underlying fact: stablecoin provision is being provided by balance-sheet constrained intermediaries that act in multiple different countries. When there’s more demand for currency conversion in country B, that intermediary shifts its provision away from country A, which will create parity deviations in country A, even though nothing in country A has changed. In other words, there is limited conversion capacity, so shifts in global conversion demand exogenous to country A will result in parity deviations there. Hence what they term “cross-market spillover” effects.

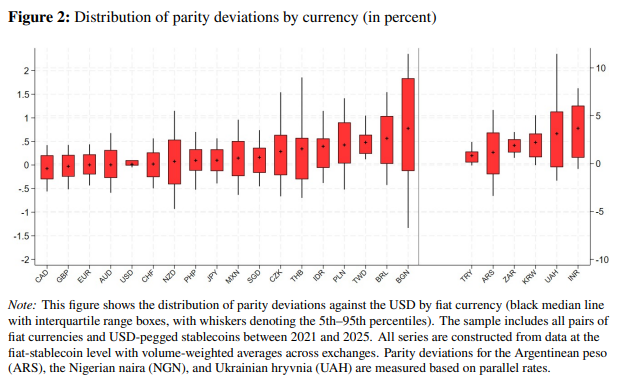

It turns out that parity deviations (reminder: when local currency price in stablecoins ≠ the price in fiat dollars) are commonplace. Here’s a nice chart from the paper:

Particularly relevant for policymakers, the researchers find that stablecoin inflows are correlated both with these deviations and with local currency depreciation (a finding I have uncovered in a case study in my own forthcoming research). The authors suggest that this, “provides suggestive evidence that flows into stablecoins are not confined to the crypto ecosystem but can generate tangible pressures in traditional FX markets, potentially by increasing the net supply of the local currency in the spot market as users sell local currency to buy stablecoins.” As the authors note, endogeneity is a concern here: if you think the local currency is going to depreciate, you’d probably move into stablecoins (seemingly the case in my case study, but not necessarily true everywhere, as they show with their causal identification strategy).

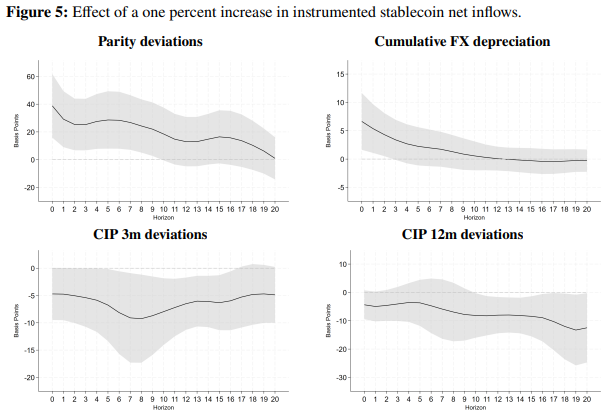

To get causal ID, they need to do some fancy causal inference stuff, which they do with a special type of instrumental variable. Sparing the detailed empirics thereof, let’s stipulate that they can identify exogenous stablecoin flows, and they find that they matter a sizable amount (horizon is in days):

Here’s the big takeaway, per the authors (citations omitted, emphasis added):

A positive shock to stablecoin inflows causes an immediate, sharp increase in parity deviations of approximately 40 basis points on impact. This effect is highly persistent, decaying only gradually over the following ten days. The persistence of these deviations is consistent with impaired arbitrage of the type that characterizes segmented markets.

Stablecoin inflows also lead to a statistically significant depreciation of the local currency in the traditional spot market. The magnitude of the effect declines over time and loses statistical significance after a few days. This confirms that shocks originating in the stablecoin market spill over into traditional FX markets, exerting tangible pressure on the local currency.

Finally, the shock to stablecoin inflows causes a significant decline in 3-month CIP deviations, indicating a deterioration in synthetic funding conditions (a higher dollar premium). In contrast, the effect on 12-month CIP deviations is negligible in the short-term and statistically insignificant. This tenor-specific pattern suggests that arbitrageurs’ constraints are more binding at shorter horizons, making short-term CIP deviations more sensitive.