Dollar Check-in: Argentina Swap, Yen

a check in on America's FX policy

You’ve all heard the macro joke—there are four kinds of economies in the world: emerging, advanced, Argentina, and Japan. Let’s start with Argentina, and then Japan.

Argentina: What happened with the swap?

So, we have the New York Fed/Treasury FX Operations Report for October–December 2025 (hereafter Report), which I’m just now taking a look at. There’s one very interesting part, which discloses some important bits of the Argentina ESF swap drama we talked about earlier. To recap, the United States provided Argentina a $20 billion swap line through the Treasury’s ESF in September 2025. This is different from central bank (Fed) swap lines, and that’s an important distinction to remember because the operational executor of both types of swaps is the New York Fed (as trading desk for the Federal Reserve and as fiscal agent for the Treasury). Anyways, here’s the Easter egg from the Report (my emphasis):

During the weeks following the local elections, Argentine financial markets faced acute, short-term pressure on both the exchange rate and financial stability. Against this backdrop and in order to stabilize Argentine markets and preserve exchange rate stability, in October 2025, the U.S. Treasury, acting through the Exchange Stabilization Fund (ESF), purchased Argentine pesos in the spot and Blue Chip Swap markets and entered into an exchange stabilization agreement (ESA) with the Central Bank of Argentina (BCRA) for $20 billion. Pursuant to the ESA, in October 2025 the U.S. Treasury, acting through the ESF, and the BCRA executed a swap transaction whereby the BCRA exchanged pesos for $2.5 billion. In December 2025, the BCRA fully repaid the $2.5 billion swap transaction when it matured and the swap transaction was closed. As of end December 2025, no drawings were outstanding under this agreement and the ESF did not hold any pesos.

So, first of all, this is still weird. As we suspected in the earlier note on this, the intervention was at least partially driven by ideological affinity for Mr. Milei’s politics, and this report is pretty clear about that, citing the local elections Mr. Milei’s party faced. If you swapped in Malaysia for Argentina, everyone’s eyebrows would be raised.

Second, we got disclosure of the direct (and derivative) peso purchases. We don’t know how many were purchased, but we know they unwound the transactions pretty quickly. Third, we got the swap amount disclosed: $2.5 billion of $20 billion available for no more than ~3 months. The BCRA disclosed the operation and its conclusion two weeks ago. We also know that, after obtaining $2.5 billion through the Treasury swap, the BCRA, on January 7, 2026, obtained $3 billion by borrowing in the repo market against its dollar-denominated bonds, evidently to make a bondholder payment coming due on January 9.

The other bit I missed that happened in October was that the US provided Special Drawings Rights (SDRs) to Argentina so that it could make an interest payment to the IMF (if you don’t know what SDRs are, check out the primer). (Somewhat confusingly, a CRS report said that the US provided “dollar liquidity support to Argentina through transactions in international reserve assets held at the IMF,” but in fact the transaction was a sale of SDRs from the US perspective in exchange for dollars.)

From the October 2025 ESF Financial Statement (my emphasis):

The Special Drawing Rights Act of 1968 authorizes the United States to purchase, sell, and hold Special Drawing Rights (SDRs) through the Exchange Stabilization Fund "ESF". In October 2025, Treasury, through the ESF, sold SDR 641 million to Argentina in exchange for $872 million. The proceeds from the sale were invested in Nonmarketable U.S. Treasury Securities. As of October 31, 2025, U.S. SDR Holdings were SDR 127 billion. Changes in both SDR Holdings and SDR Allocations reflect changes in the foreign exchange rate.

So, my read is that (1) in October the BCRA draws ($2.5 billion) dollars from the ESF swap; and then (2) swaps back $872 million of that for SDRs to make its IMF payments; and finally (3) unwinds the swap transaction in December.

I don’t know, I can’t keep up with Argentina, but it looks like this has settled for now (?). Will we get more details on the ESF swap? Why didn’t the BCRA use it for the $3 billion it got from the repo market? What’s the rate on this thing?

Tokyo Drift?

If you were unfortunate enough to be on X (the artist formerly known as Twitter) or, even worse, LinkedIn, late last month, you’d know that folks online were talking about the New York Fed performing “rate checks” on USDJPY. (I even saw one crypto person claim, incredibly, that the Fed might “crash the dollar by 50%.”) Rate checks are basically when a central bank asks to get quotes on an exchange rate from commercial banks, sometimes allowing or instructing them to let the market know they might be mulling an intervention (i.e., to some degree jawboning the exchange rate). Now that we have the minutes from the January FOMC meeting, we do have the disclosure of this happening (my emphasis):

In the days leading up to the meeting, the dollar had depreciated markedly after reports that the Desk had made requests for indicative quotes, known as "rate checks," on the dollar–yen exchange rate. The manager noted that the Desk had requested those quotes solely on behalf of the U.S. Treasury in the Federal Reserve Bank of New York's role as the fiscal agent for the U.S.

And then, Scott Bessent said the US would “absolutely not” intervene in the yen and reiterated the time-tested strong dollar policy. Oh well, so much for the drama. Hopefully nobody reading this got caught going the wrong direction in a USDJYP trade (sorry if you did, it seemed reasonable). So, what is Treasury’s dollar policy?

Nothing much happens

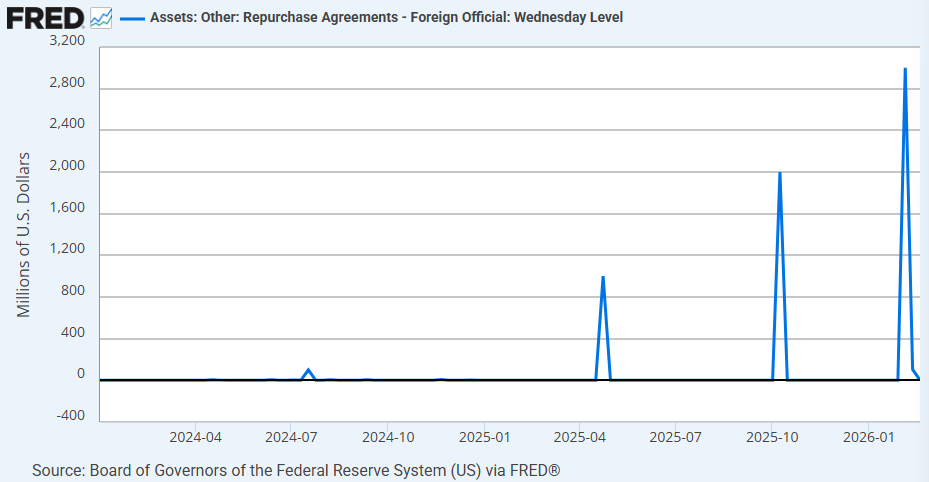

Things in the rest of the world seemed quiet, according to the Report. We’ll all be glad to hear that offshore dollar funding markets are in rude health. Carry traders are at it again in EMs. One other interesting thing happened recently, though, outside of the Report at hand: there was some FIMA Repo activity: balances were up in the first week of February to $3 billion. Here’s a chart:

I am unaware of any public reporting on this or any chatter, so my guess would be that this recent draw was pretty routine—if so, good to know the pipes still work.