Political Economy and the Fed's Operating Framework

separating fact from fiction

A central bank’s operating framework (read: the tools it uses to implement monetary policy) is rarely the subject of public controversy. Recently in the US, though, the proverbial town square of academia and policymakers has been awash with discussions of the Fed’s operating framework, not least because some identify the framework as a primary or partial cause of considerable losses in recent years. Herein, I will engage with a few of the major lines I’ve heard repeated (in various venues) and offer some thoughts.

Fair warning: this article assumes some technical knowledge of the Fed’s operating framework. If you want to get up to speed on that, I recommend checking out this short primer.

IORB: Subsidy to the banking industry?

Fact or fiction: Since the Fed pays interest on reserves balances of commercial banks, and those reserves are risk-free, isn’t the Fed providing a subsidy to the banking sector, insofar as it’s essentially handing out risk-free revenue to commercial banks? Moreover, it doesn’t have to do this—the Fed operated zero interest on reserves policy (ZIRP) for the vast majority of its existence. Worse still, since interest payments on commercial bank reserves are a cost/expense to the Fed, mechanically reducing what it pays to the Treasury, doesn’t it then follow that taxpayers are indirectly paying for this banking sector subsidy?

Answer: Fiction (given the bank capital requirements that exist).

Many people, including some senators, are very upset about this arrangement. I have heard interest on reserve balances (IORB) described in vivid terms as a serious subsidy to the banking sector at taxpayer expense. This argument is popular, but misguided.

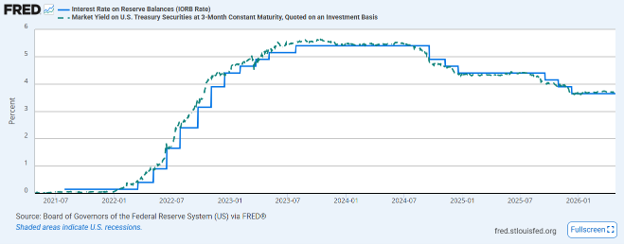

First, paying interest on reserves does not obviously result in a cost to the Treasury. IORB is an expense on the Fed’s income statement, mechanically reducing profits flowing to the Treasury in an accounting sense. By this logic, indeed IORB does cost the Fed. Alas, one must consider the alternative: because banks must, for regulatory purposes, hold High Quality Liquid Assets (HQLA), and there are no binding reserve requirements, banks would need another risk-free HQLA asset with positive yield to hold for regulatory purposes—Treasury securities. In other words, removing IORB would go hand-in-hand with a return to a scarce-reserves framework,1 in which banks would hold Treasury securities instead of reserves, which would shrink the Fed’s balance sheet. Short-term Treasury securities yield about the same—typically a bit more—than reserves at the Fed:

In this sense, the fiscal cost would be the interest on Treasury securities, a direct taxpayer cost. It would likely be a wash, but if Treasury yields are higher than IORB (in other words, in an upward-sloping yield curve world), then the fiscal cost would in fact increase, not decrease.2 This is a fact that even Stephen Miran, a Trump appointee to the Board of Governors and frequent Fed critic, acknowledged in a recent speech at the Bank for International Settlements, noting that it is only optics that differ with respect to IORB (emphasis added):

A consequence of the Fed’s large balance sheet is significant payments of interest to the banking sector. Now, this is little different for banks’ income than if they held Treasurys directly, as would occur in a scarce-reserves regime. In fact, an upward-sloping yield curve would suggest banks would earn more from holding Treasurys rather than reserves. Regardless, the optics differ. Large interest on reserve balances (IORB) outlays may appear like the Fed is unfairly subsidizing the banking system with billions of dollars, even if that’s not the case. These perceptions can affect the Fed’s credibility and thus its effectiveness. Several times now, the Senate has debated whether the Fed ought to be stripped of its statutory authority to pay IORB despite its necessity as a tool for managing the federal funds rate.

Governor Miran has identified the primary challenge of IORB in the political economy arena: it creates the perception that IORB creates a net taxpayer cost, even while in economic fact it makes little difference (and in the long run probably costs the taxpayer less). There is also a relationship between IORB and the Fed’s net profit margin related to its income-producing assets. While the Fed’s profits (or losses) are an incomplete unit of analysis for net fiscal cost, this mechanism is worth considering. Reserves represent one of the Fed’s sources of balance sheet funding. If IORB is lower (higher) than the yield on assets it owns, then it supports positive (negative) net interest margin for the Fed and drives profits (losses). In the long run, this net interest margin should average to around zero (as the Fed holds assets whose maturities approximate its liabilities) or moderately positive.3 If for whatever reason policymakers wished to lower the Fed’s interest expenses on IORB, they could do so without jettisoning an effective monetary policy implementation tool by adopting a tiered reserves system (as numerous central banks currently do) and remunerating only reserves above a certain threshold.

Second, paying interest on reserves does not obviously create a windfall for banks. Banks have to fund reserves with deposits or other borrowing, as they do for all other assets; short-term borrowing costs are little different from IORB. This of course varies over time. In Q4 2025, per the FDIC’s Quarterly Banking Profile, the average US bank cost of funding earning assets was 2.15% versus IORB which averaged 3.92% during that period. However, in Q4 2021, the average funding cost was 0.17% versus IORB of 0.15%. In the long run, banks’ average cost of funding should be moderately higher than IORB since their average funding cost represents a weighted average cost of funding that will be persistently above an overnight maturity and involves credit risk. In other words, while there will be intertemporal variation, in the long run, it should be close to a wash. It is therefore no mystery that while the Fed’s IORB payments soared, banking system profits were more or less unchanged.

Forcing banks to hold reserves and not remunerating them during ZIRP was an implicit tax on banks. To be sure, banks do use and benefit from Fed services (e.g., payments clearing), so this implicit fee may be a reasonable fee to levy, but we should be clear that that’s what it is. This implicit tax was presumably passed along to consumers, who are normal taxpayers like individuals and businesses, and also resulted in distortive and wasteful bank behavior to avoid the tax. In addition to better monetary policy implementation, these were among the reasons that the Fed moved away from ZIRP.4

The bottom line is that a move away from IORB would result in just as much, if not likely more, fiscal cost than IORB, given the alternative scarce-reserves framework and existing regulatory environment. It is the regulatory environment that is the binding constraint, a phenomenon that Governor Miran has termed “regulatory dominance” of the Fed’s balance sheet. So long as liquidity and capital regulations are more or less unchanged, there will be some “fiscal cost,” if you wish, to the implementation of monetary policy. Moreover, a move away from IORB would not obviously represent a cost to banks, which would likely find their net interest margins unchanged.

QE: Taxpayer losses?

Fact or fiction: Since the Fed (1) bought a bunch of assets in QE that it has now made losses on; and (2) pays more (at least until recently) on its liabilities than it does the assets it acquired in QE, thereby making income losses, isn’t it the case that QE has been a net fiscal cost to the taxpayer because of the valuation and income losses the Fed has suffered because of it?

Answer: Almost certainly fiction (but the magnitude is hard to quantify).

QE is a lot of things, but it should certainly win the award for most controversial Fed (or central bank in general, really) policy in recent decades. There’s a lot to talk about with QE, but I’ll focus here on the question of whether QE-induced Fed losses are a net fiscal cost to the taxpayer.

The narrative for why it would be a fiscal cost is laid out above. In short, the Fed has made losses, through two channels: First, it bought assets when rates were low,5 so as interest rates rise, it suffers mark-to-market valuation losses. Second, the Fed pays interest on reserves at a higher rate than it receives interest on the assets it owns (again, by construction), so this results in negative net interest margin.

The total fiscal calculus of QE, though, must account for the three primary fiscal channels through which it works: (1) the effect of Fed losses (or profits) it remits to Treasury; (2) the reduction in Treasury debt servicing costs it creates; and (3) the stimulation of economic activity it engenders (which raises tax revenues). This is not to say that fiscal calculus is straightforward, but it does outline the necessary ingredients for a thorough analysis: a consolidated government balance sheet view.6

An analysis by the nonpartisan Congressional Budget Office (CBO) in 2022 entitled How the Federal Reserve’s Quantitative Easing Affects the Federal Budget, authors conclude (my emphasis):

The net budgetary effects over time of the combined QE and QT [quantitative tightening] policies are uncertain . . . . the effect of QE on the budget in the short run depends on the gap between economic output and potential output. The net effect of balance sheet expansions on the nation’s finances over the long run is difficult to assess and may be positive, negative, or neutral.

Specifically on the question of mark-to-market losses on government bonds (the vast majority of assets purchased by the Fed during QE), we’re again back to neutral on the consolidated government balance sheet. Enter Cecchetti and Hilscher (2024) (my emphasis):

Losses from mark-to-market declines in the value of its government bond holdings do not appear on the consolidated balance sheet of the government. The losses of the central bank are the gains of the fiscal authority, so they are an internal government transfer.

So, we’re left with two countervailing forces here. First, QE losses from government debt assets (substantially all of them) are a wash for the consolidated government, so the magnitude of losses (or gains for that matter) don’t enter into fiscal cost calculus at all. Second, whatever real negative income costs the Fed suffers need to be offset against (1) the growth in the economy QE engenders, and (2) the reduction in Treasury financing costs QE engenders. The CBO study concluded that QE episodes in response to the Global Financial Crisis and the COVID-19 pandemic “initially reduced federal deficits” (emphasis added), while noting that the long-run effects were more uncertain. In other words, it’s very difficult to say.

One must adopt heroic faith in dynamic stochastic general equilibrium models and/or ex post causal inference techniques to have strong convictions on the net budgetary effects of QE in either direction. Simply not knowing the net budgetary effects of QE is perfectly acceptable—indeed the CBO implicitly said that estimating it was too thorny a causal inference problem to tackle. The honest answer about the exact fiscal impact of QE is that we’re not 100% sure, but it’s almost certainly not a net cost.

TGA: Taxpayer subsidy to the Fed?

Fact or fiction: Since the Treasury parks its money at the Fed (instead of at commercial banks) and earns no interest on its deposits, isn’t it providing the Fed a windfall zero-cost liability, essentially loaning the Fed money interest-free, which is a form of subsidy?

Answer: Fiction.

It is true that the Treasury General Account (TGA) is a cost-free liability to the Fed, and cost-free liabilities do mechanically reduce losses in an accounting sense (by simply lowering expenses). So, it is tempting to see the TGA as a backdoor bailout for the Fed. But that is a misleading picture.

From the standpoint of the consolidated balance sheet of the government—the unit of analysis for net fiscal cost—it’s a wash: paying interest on TGA reserves would just be one part of government paying another. This is a point recently made by Governor Miran when discussing the idea of paying interest on the TGA: “it’s a wash on the consolidated government balance sheet; reducing the Fed’s net profits also reduces remittances to Treasury.” Put another way, the Treasury paying interest on the TGA would just be the left hand paying the right. Adding interest to the TGA would be a trivial accounting exercise with no impact on the consolidated government’s balance sheet.

This might matter for optics, but in economic reality paying interest (or not) on the TGA makes no difference to the fiscal-cost calculus.

Fed-Treasury Relationship: Debtor-Creditor?

Fact or fiction: Since the Fed has been running losses and not making remittances to the Treasury, but continues to pay IORB as well as operating expenses (pensions, salaries, etc.), isn’t the Fed essentially borrowing money from the Treasury to stay afloat?

Answer: Mostly fiction, although there’s something to this view.

This would only be effective borrowing if the Treasury were “owed” those remittances and was extending a line of credit to the Fed. When the Fed makes negative profits, it is not functionally borrowing from the Treasury. It does not have a legal requirement to make unconditional remittances; therefore, no money is owed and, as a result, no effective borrowing takes place. It’s simply not making remittances. The law on this issue is clear: the Federal Reserve Act (as amended) (§7a) simply indicates that the surplus of the Reserve Banks over a threshold ($6.825 billion) must be transferred to the Treasury; it says nothing at all about any legal requirement that the Fed provide surpluses above that threshold or indeed operate with any surplus at all. An accurate description of the Fed’s (contingent) liability to the Treasury is a stepwise function: if the Fed makes negative profits, there is no liability toward the Treasury; if the Fed makes profits but those profits accrue to less than $6.825 billion, there is no liability toward the Treasury; if the Fed makes profits and those profits accrue to more than $6.825 billion, then a liability to the Treasury is created in the amount of the Federal Reserve System’s total accrued profits less $6.825 billion.

The 2026 version of the Financial Accounting Manual for Federal Reserve Banks (§11.96—Accrued Remittances to Treasury / Deferred Asset) states (my emphasis):

A credit balance in this [Treasury remittances] account represents the accrued remittances to be distributed to the Treasury. If a Reserve Bank’s earnings become less than the costs of operations, payment of dividends, and maintaining surplus at an amount equal to the Bank’s allocated portion of the aggregate surplus limitation, remittances to the Treasury would be suspended. A deferred asset is recorded in this account, and this debit balance represents the amount of net excess earnings the Reserve Bank will need to realize before remittances to the Treasury resume.

The Fed does not need to borrow from Treasury, either literally or effectively, to make payments on IORB or ONRRP or to pay salaries or operational expenses; as a central bank, it can create the funds to do so (to the limit of creating inflation and compromising on its mandate, to be sure).

Broadly speaking, it is true that, all else equal, fewer Fed remittances to Treasury require the Treasury to increase borrowing (or taxes). But, as noted elsewhere in this essay, not all else is equal: losses from, for example QE, could well be offset by the higher tax revenues and lower interest expenses for the Treasury that it has engendered.

But abstracting from the narrow strictures of the Fed’s specific legal foundations, it is true that, in the limit, the central bank cannot use money creation to fund its operations and framework without creating costly inflation. In this sense, if the central bank has considerable negative equity and wants to operate non-inflationary monetary policy, it would need a capital infusion, which would be provided by the Treasury (or member banks). This is recognized in the Bank of England’s relationship with HM Treasury, and explicit in its operating framework (see BoE-HMT Memorandum of Understanding, pp. 8–10). In the (more likely) case that the Treasury is the capital provider, this relationship would be similar to, but distinct from, a debtor-creditor relationship; the Treasury’s role would be more akin to that of a callable capital provider of last resort. Again, this is essentially the British setup.

In the case that the Treasury had to legally recapitalize the Fed for its losses, the net fiscal effect would still be zero, as noted in Cecchetti and Hilscher (2024), citing Buiter (2008):

Recapitalization of a central bank is in essence a trivial transaction within the government in which the fiscal authority can simply exchange government bonds for central bank equity. As we will see below, this has no impact at all on the consolidated balance sheet of the government. But if one separates the two balance sheets, it does recapitalize the central bank.

Upshot: Partial vs. general equilibrium strikes again

The partial vs. general equilibrium debate is as relevant in central banking policies as it is in any other economic question. In this setting, it manifests as a question of the central bank balance sheet in isolation vs. the central bank balance sheet as part of the consolidated government balance sheet; it is the latter that is informative about true fiscal costs. That is a matter of accounting mechanics and legal truths, but it is equally true in the economic sense: should the Fed execute a policy that costs taxpayers n dollars on its balance sheet and saves them n dollars on the Treasury’s balance sheet, the net fiscal cost is zero. Or, similarly, if the Fed executes a policy that costs taxpayers n dollars, but that the Treasury would otherwise be doing (e.g., IORB vs. Treasury payments on bills and bonds), then the Fed is adding no fiscal cost relative to the baseline. These interplays and netting effects are lost when one focuses on the partial equilibrium of the Fed’s balance sheet in isolation.

What is certainly true is that stakeholders of the Fed—informed citizens, the financial industry, and most importantly policymakers and elected officials—must understand the tradeoffs inherent in monetary policy operating frameworks. The Fed could, and should, do a better job of explaining these frameworks to the public.

Alternatively, the Fed could rely more on repo-based facilities to set a floor on interest rates but, from an expense perspective, this is effectively the same as IORB.

For reference, in the five years from April 2021 to April 2026, the average spread between IORB and the three-month Treasury bill yield was 8.2 basis points. In the long run, the spread should ultimately average to be slightly negative (since IORB is overnight and T-bills are three-month). See Federal Reserve Bank of St. Louis (link).

The reason it might settle at a long-run moderately positive margin is that the Fed’s liabilities include some non-interest-bearing liabilities, like currency in circulation, which should drive its weighted average interest cost lower than its weighted average interest revenue.

QE aside, the Fed considered numerous other operating frameworks before selecting the ample reserves framework in 2019. Effective rate control, simplicity, and robustness to funding shocks are among the major reasons that most advanced economy central banks now operate with ample reserves. See Julie Remache, Balance Sheet Reduction and Ample Reserves, Speech (Federal Reserve Bank of New York, 2025), https://www.newyorkfed.org/newsevents/speeches/2025/rem250929.

This is, of course, the point: the central bank engages in QE precisely when it approaches the effective lower bound. A more nuanced point that often gets missed is that, for all those who don’t like the central bank doing this, the fiscal authority (Treasury via Congress) could do this too. This is the subject of the now famous “stealth QE” debate: the Treasury could essentially change its issuance structure to issue more at the front end of the curve and buy back longer-maturity debt. This is a problem for keeping issuance predictable, so there’s a reason fiscal authorities don’t generally engage in this, but the point is that you don’t strictly need a central bank to do QE.

For a helpful visual of the consolidated balance sheet of the public sector, see Table 2 in Stephen G. Cecchetti and Jens Hilscher, Fiscal Consequences of Central Bank Losses, NBER Working Paper Series Working Paper No. 32478 (2024), 8, https://www.nber.org/system/files/working_papers/w32478/w32478.pdf.