Primer: The SDR and Its Discontents

a brief primer on Special Drawing Rights and the debates surrounding them

From time to time, I get asked “what my understanding of SDRs” is, which is a kind of funny way to ask a question, intimating that my interlocutors themselves might also struggle with the question. I tend to hesitantly respond myself. SDRs are just kind of arcane. I figured it would be useful to talk about here, because it’s an interesting topic in the global economy/financial system/development space/international political economy of the world (plus, they come up a fair bit in emerging market macro stuff, particularly with respect to concessionary development financing and central bank reserves).

IMF Funny Money

You may or may not have heard of Special Drawing Rights (SDRs), the IMF’s own unit of account and awkward stepchild of bancor, [1] Keynes’ proposal for a supranational currency at the Bretton Woods conference. To start with what they’re not: SDRs are not a currency, like a dollar or euro or whatever. And they are not bancor.

SDRs are an interest-bearing reserve asset that serve as the IMF’s unit of account and represent contingent claims on the following currencies (“hard” currencies): the dollar, the pound, the euro, the yen, and the renminbi. They can be used to settle accounts with the IMF, but cannot be used to buy and sell goods or services. The IMF can create—and, in theory if not practice—destroy SDRs. When SDRs are created, they are created proportional to each nation’s quota in the IMF.

Here’s the IMF (links omitted, emphasis mine):

The Special Drawing Right (SDR) is an interest-bearing international reserve asset created by the IMF in 1969 to supplement other reserve assets of member countries.

The SDR is based on a basket of international currencies comprising the U.S. dollar, Japanese yen, euro, pound sterling and Chinese Renminbi. It is not a currency, nor a claim on the IMF, but is potentially a claim on freely usable currencies of IMF members. The value of the SDR is set daily by the IMF on the basis of fixed currency amounts of the currencies included in the SDR basket and the daily market exchange rates between the currencies included in the SDR basket.

SDRs are only allocated to IMF members that elect to participate in the SDR Department. Currently all members of the IMF are participants in the SDR Department.

SDRs can be held and used by member countries, the IMF, and certain designated official entities called “prescribed holders” []—but it cannot be held, for example, by private entities or individuals. Its status as a reserve asset derives from the commitments of members to hold and exchange SDRs and accept the value of SDRs as determined by the Fund. The SDR also serves as the unit of account of the IMF and some other international organizations, and financial obligations may also be denominated in SDR.

Only members that are not participants in the SDR Department, non-members, and official entities may be prescribed as holders of SDRs . . . [2]

So, to be clear, an SDR is a “claim on freely usable currencies of IMF members”; read: they’re claims on dollars, euros, pounds, yen, and renminbi. Their value is a weighted average of those currencies:

source: IMF

Similar to interest-bearing central bank reserves, interest is paid on SDR holdings [3] at the SDR interest rate (SDRi), which is calculated based on the government debt of the issuers of those currencies:

source: IMF

A clunky analogy is to poker chips. They’re kinda funny money, but they’re definitely not nothing (you’d get hauled away for stealing someone’s poker chips in a casino!). They are a unit of account and they represent an asset the casino owes you, or you owe other players, or whatever. They represent claims on real hard currency, even if they themselves cannot be used in (most) transactions (except for those within the casino) and are not themselves hard currency. If your net worth is $100,000 and you go to a casino and play poker with $70,000, your net worth is not suddenly $30,000 because 70% of it is now in poker chips: the poker chips count. But at the same time, you can’t buy a coffee with poker chips. You need to exchange them at a fixed exchange rate back into hard currency you can use to settle transactions with actors outside of the casino. In fact, in some online casinos, you might even buy poker chips using one currency and cash out into another currency—that’s fine too, so long as the exchange rates are clear ex ante.

The chips have a fixed exchange rate in hard currency terms and serve as a unit of account and means of settlement within a defined environment (the casino) and only for specific transactions (e.g., even within the casino, you’re not buying your drinks with chips), but otherwise must be liquidated into hard currency to be useful. And they are not like gold: there is a (mostly) fixed supply of gold in the world, so while it might be tempting to analogize SDRs or poker chips to gold, it’s not really the same thing. The quantity of poker chips in circulation in a casino is a function of (1) the net worth of the players in the casino and (2) how much of that net worth, in hard currency, they’re willing to exchange for poker chips. [4]

The critical thing about the poker chips though is that there is an explicit promise of the casino to exchange your chips into hard currency. Similarly, the liquidity and usefulness (aside from transacting directly with the IMF—not nothing) of SDRs is underpinned by the willingness of those nations or currency unions (Eurozone) whose currencies comprise the SDR basket to exchange SDRs for their currencies. In other words, if I’m a country and I have a bunch of SDRs and I’d like to do something with them (buy COVID-19 vaccines, for example), then for the SDRs to be useful, I need to be sure I can exchange them into dollars, euros, pounds, yen, or renminbi, because, remember, you can’t buy or sell goods and services with SDRs—only hard currencies. Again, like poker chips, they count for something, but you have to be able to convert them into real hard cash to go buy your coffee.

Enter the Voluntary Trading Arrangement, the market supporting the SDR’s hard currency liquidity. Here’s the IMF (emphasis mine):

For more than three decades, the SDR market has functioned purely on a voluntary basis.

Various Fund members and one prescribed SDR holder have agreed to stand ready to buy and sell SDRs on a voluntary basis.

The Fund facilitates transactions between members seeking to sell or buy SDRs and these counterparties to the voluntary arrangements that effectively make a market in SDRs. Under the guidance of the Fund, participants in the SDR department can also enter into bilateral transactions amongst themselves or with prescribed holders.

In the event that there are not enough voluntary buyers of SDRs, the IMF can designate members with strong balance of payments positions to provide freely usable currency in exchange for SDRs. This so-called "designation mechanism" ensures that a participant can use its SDRs to readily obtain an equivalent amount of currency if it has a need for such a currency because of its balance of payments, its reserve position, or developments in its reserves. The designation mechanism has not been activated since 1987.

So, a country holding SDRs might sell them to an IMF member or a prescribed holder for hard currency. Example: I’m Jamaica, and I just stumbled upon some SDRs (more on that later). I could do some IMF-y stuff with those SDRs (like pay back some debts to the IMF for borrowing I did a few years ago). I could just hold onto them, because why not, they’re reserve assets like gold or dollars or whatever. But maybe I’d like to buy some stuff (e.g., vaccines). Here’s what that would look like:

source: IMF

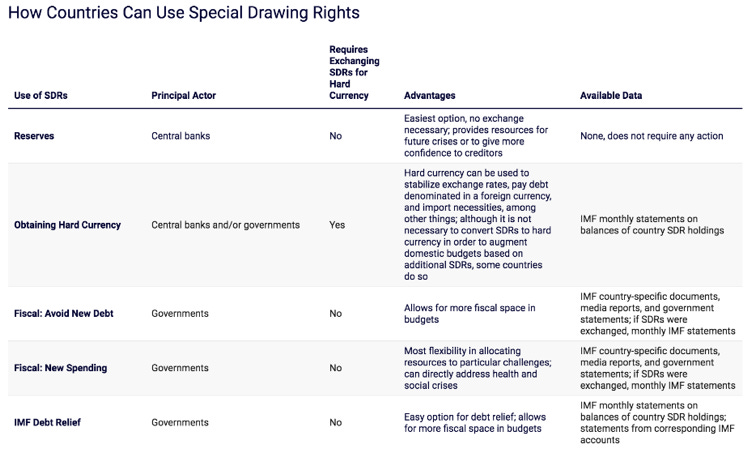

But again, one doesn’t have to convert them into hard currency. There are a number of things [5] one could do with SDRs, outlined nicely by some leading scholars in the field:

source: Cashman, Arauz, and Mehrling 2022

But where do they come from? Similar to the poker chips in the casino, they’re created in proportion to the money the members/players bring in. IMF members vote to “allocate” (create) SDRs, and when they’re created, they’re allocated in proportion to a member’s quota in the IMF. (Theoretically, the IMF can also vote to destroy SDRs, though historically it’s never done so.)

This has happened a few times over the lifetime of the IMF, most recently during the COVID-19 crisis:

source: IMF (n.b., in nominal values)

Idle Hands Doing Nobody’s Work?

Folks are generally not all that happy with the state of SDR affairs. SDRs are sometimes viewed as unproductive and regressive, redistributing from the rich to the rich, if redistributing at all. In my humble view, this perhaps doesn’t give SDRs enough credit and overlooks the “plumbing” challenges (getting existing unused SDRs held by rich countries to the places they’re needed most) as the key issue (as opposed to allocation). But irritation with the way SDRs are (under)used is pretty broad-based at this point.

To their critics, the two primary (and related) issues with SDRs are that (1) they go to precisely the countries that don’t need them; and (2) partially as a result of (1), they basically just sit on the balance sheets of large countries and don’t do anything.

I’m not going to discuss (1) much here in isolation, since it’s not within the political reality of the world as it currently exists to change, but the rough framing is that SDRs (contingent claims on the currencies of select rich nations) should not be allocated proportionally to quota share, but should go to the countries that need them most. Idea is: (i) create some SDRs, thereby creating contingent liabilities [6] on the balance sheets of a few rich countries; (ii) give those SDRs to poorer countries that need them more; (iii) as a result of (i) and (ii) combined, those few rich countries have incurred a larger net contingent liability [7] to the rest of the world—in effect, a larger transfer from the moment of SDR creation. There are obvious political problems with this approach and my read is that it’s not a serious policy option on the table anytime soon.

The second—I think probably more interesting—concern is that rich/surplus nations get lots of SDRs, don’t need them, know that they don’t need them, and then do very little with them, leaving the needier countries understandably peeved. In other words, given that:

the IMF’s purpose is to support global monetary stability—a mission the SDR basket currency-issuing countries formally support;

the entire point of SDR allocations is in pursuit of that goal;

those SDR basket currency-issuing countries knew and supported that goal ex ante in their vote supporting those allocations, thereby implicitly (and sometimes explicitly) supporting the idea that the newly created SDRs would make it to the countries most in need,

then, like, why aren’t they doing stuff with their SDRs? If you didn’t want to support the creation of SDRs and sending them to countries in need, why did you vote for their creation in the first place? If you don’t like the idea of creating contingent liabilities on your balance sheet to provide hard-currency liquidity to low-income countries, then . . . just don’t? It seems weird to support the creation of SDRs and then oppose doing anything useful with them. That’s all a bit of a straw-man characterization of course, and there’s a lot more nuance going on that I’m admittedly skipping over, but I think that captures, in very broad strokes, the source of discontent.

In this vein, Stephen Paduano and Brad Setser have called SDRs, an “ambitious but woefully underused reserve asset” that “sit[s] idle on the balance sheets of high-income countries.” Cashman, Mehrling, and Arauz say that, “while more than half of an SDR allocation goes to high-income economies that do not need them, this does not lead to waste or maldistribution, because high-income countries do not use SDRs.” For many poor countries, the existence—and idleness—of vast swathes of SDRs recalls the bastardized line from the poem The Rime of the Ancient Mariner: “Water, water, everywhere, but not a drop to drink.”

SDR Recycling FTW?

I’m not going to get into the details of the numerous proposals on the table, as I wish to keep this primer somewhat succinct, but discussion of SDRs merits some overview of the various reforms on the table for getting SDRs to spring to life off their balance sheet daybeds and support the lending the world needs to finance the response to global instability, poverty, and climate change (though note here that some wonks reading this might cringe because the last two things are traditionally viewed as being the World Bank’s wheelhouse—a recurring theme). The following is not an exhaustive list, but here are a few thoughts:

World Bank SDR Bonds

Rich nations could buy SDR-denominated bonds issued by the World Bank, thereby swapping their SDRs for a bond that pays them interest and providing funding to the World Bank in the process.

This setup would preserve the reserve asset quality of SDRs—which is critical to maintain—while putting them to better use. They’d still get paid for their holdings (potentially exactly the same, if the bonds paid the SDRi rate), and they’re still reserve assets, but the SDRs get used.

The proceeds from these bonds would then fund the World Bank and allow it to do more critical lending, particularly if issued as subordinated debt, which would comprise capital for the World Bank, allowing it to stretch its balance sheet further.

This idea has been floated by Brad Setser and Stephen Paduano, see here.

SDRs for Hybrid Capital

Similar (but distinct) to the World Bank SDR bond proposal, the IMF recently approved a proposal to allow SDR holders to use SDRs to purchase hybrid capital in multilateral development banks.

Similar to the advantages of the World Bank bond proposal, such a framework could maintain the reserve asset qualities of SDRs, while putting the SDRs to much greater use.

For reasons we may explore elsewhere, this proposal is unlikely to go anywhere despite formal approval, which is interesting on its own merits. In short, the proposal is plagued by a network problem: it works if lots of countries participate, but fails to work when only a few countries sign up (an asset isn’t very liquid when only a few market participants trade in it —and remember, SDRs must remain liquid to preserve their reserve asset characteristics).

Recycling à la IMF

Countries can contribute their SDRs to two IMF programs that aim to on-lend the funds to countries in need: the Poverty Reduction and Growth Facility (PRGT) and the Resilience and Sustainability Trust (RST).

In essence, this just means that IMF members can pledge their SDRs to IMF programs meant to support lending to low income countries. This is probably useful, but not all that different from rich IMF members just providing more capital for these programs writ large. And anyways, only a small portion of SDRs have been committed for this purpose thus far.

Conclusions: Critical but Criticized

SDRs are an important part of the fabric of the international monetary system, and are vital reserve assets. They are not, however, “money” as we typically conceive it, but are best understood as contingent claims on the hard currencies of the US, UK, Eurozone, Japan, and China (albeit with liquidity maintained voluntarily, for now at least). Given that they’re created in proportion to IMF quota share, they have been criticized for going to those nations that need them least. As a result, numerous proposals have been put forth to improve the efficiency of the SDR system, but it’s unclear as yet which, if any, will prevail.

If you want to discuss this further, please reach out: vincient.arnold@yale.edu. In particular, if you found this kind of primer helpful, or are interested in SDR topics, please drop me a line.

You can also follow me on Twitter (X) @ArnoldVincient, or connect with me on LinkedIn.

This work is independent from and not endorsed by the Yale Program on Financial Stability or Yale University; all views are my own.

[1] Bancor was a different proposal, to the extent that it was tied to trade: countries would pay for imports and exports using bancor at a central clearing union. The mechanics of the clearing union would in theory equilibrate the global balance of trade so that there were no major deficit or surplus countries in the long run. For more on this, see Tout at the London School of Economics.

[2] The “prescribed holders” are basically just non-country central banks (e.g., European Central Bank, Eastern Caribbean Central Bank), international monetary institutions (e.g., Arab Monetary Fund), and development groups (e.g., Asian Development Bank, Nordic Investment Bank).

[3] Technically, on surplus SDR holdings—i.e., the amount over a nation’s prescribed quota (and paid if it falls below that quota).

[4] And, in today’s world at least, while you certainly can exchange gold into almost any hard currency, you don’t have to be able to do so for it to have value (e.g., gold in Russia still has value—arguably more value—now that the Central Bank of Russia can’t exchange it for dollars on any major international exchange).

[5] Notably, one of these categories of things, per the table, is fiscal uses (whether to get on with normal government spending or to avoid new debt issuance). We may revisit this at some point because it’s kind of an interesting and under-appreciated angle: to some, this looks like monetary financing—creating money to get spent. This is indeed a controversial issue and a nuanced one, but poses real constraints on the creation and uses of SDRs.

[6] For those unclear on the terminology, a contingent liability means a liability (a “debt,” if you will) of an entity that it conditional. For example, if you have a credit card with a $4,000 credit limit, then you have a $4,000 contingent liability: you could, at any time and without any warning, accrue $4,000 in debts through a preexisting approved channel. For banks or nations, committed standby credit lines—agreements to lend up to a certain amount—are common examples of contingent liabilities.

[7] Here’s what I mean. When, for example, in the current system the US votes for the creation (allocation) of SDR 100 from the IMF, of which, let’s say, it will receive SDR 20, it books basically two entries on its balance sheet: one as a contingent liability for dollars equal to SDR 100 (since SDRs are contingent claims on dollars, along with the other four SDR currencies, and therefore theoretically everyone in the world could ask for their SDRs in dollars), and an asset equal to SDR 20, since it’s receiving SDR 20, which count as reserve assets. So, the US position (and the positions of the UK, Eurozone, Japan, and China) is one of net contingent creditor (in this example, equal to roughly SDR 80 for the US). If the system changed and the SDR allocations weren’t proportional, the net contingent creditor status of the SDR basket currency issuers would be even larger: the US supports the creation of SDR 100, books a contingent liability of SDR 100, and then receives SDR 5. Now it’s really a net creditor.