White Elephants and Paper Tigers: The Geopolitics of Chinese Central Bank Swap Lines

Not the West's bogeyman, but not the best either!

In recent years, China has expanded a sprawling network of renminbi (also known as yuan) swap lines around the world, giving monetary authorities from South America to Southeast Asia access to the redback. At the same time, the network yields geopolitical dividends, endowing Beijing with soft power heft and, at times, rivalling the International Monetary Fund’s (IMF) bailouts. Scholars, national security wonks, and at times Beijing itself, have pointed to the lines as an aid in internationalizing the renminbi, protecting China from Western1 sanctions, and fighting financial instability. Do they really live up to the hype?

What are central bank swap lines?

A central bank swap line is simply the central banker’s version of a foreign exchange swap: the two banks swap currencies with one another and agree to swap them back in the future at a pre-agreed exchange rate. This eliminates foreign exchange risk (since the exchange rate is already settled) and limits counterparty risk (since you’re dealing with a central bank). (For a more comprehensive overview, I’ve written a primer.) Swap lines have been used for decades and were historically the means of choice for foreign exchange intervention. Today, though, they’re primarily liquidity tools. The US used them to great effect in the Global Financial Crisis to get dollars to European commercial banks exposed to dollar-denominated mortgage assets.

China’s network of swaps

Most swap lines are between developed economies (the biggest network is between the US, Japan, European Union, United Kingdom, Canada, and Switzerland). This works nicely because everyone’s risk exposure is relatively small. There are some other major networks (e.g., the Chiang Mai network in Southeast Asia, borne of the 1997 Asian Financial Crisis), but they all more or less focus on getting liquidity where it’s needed to calm markets.

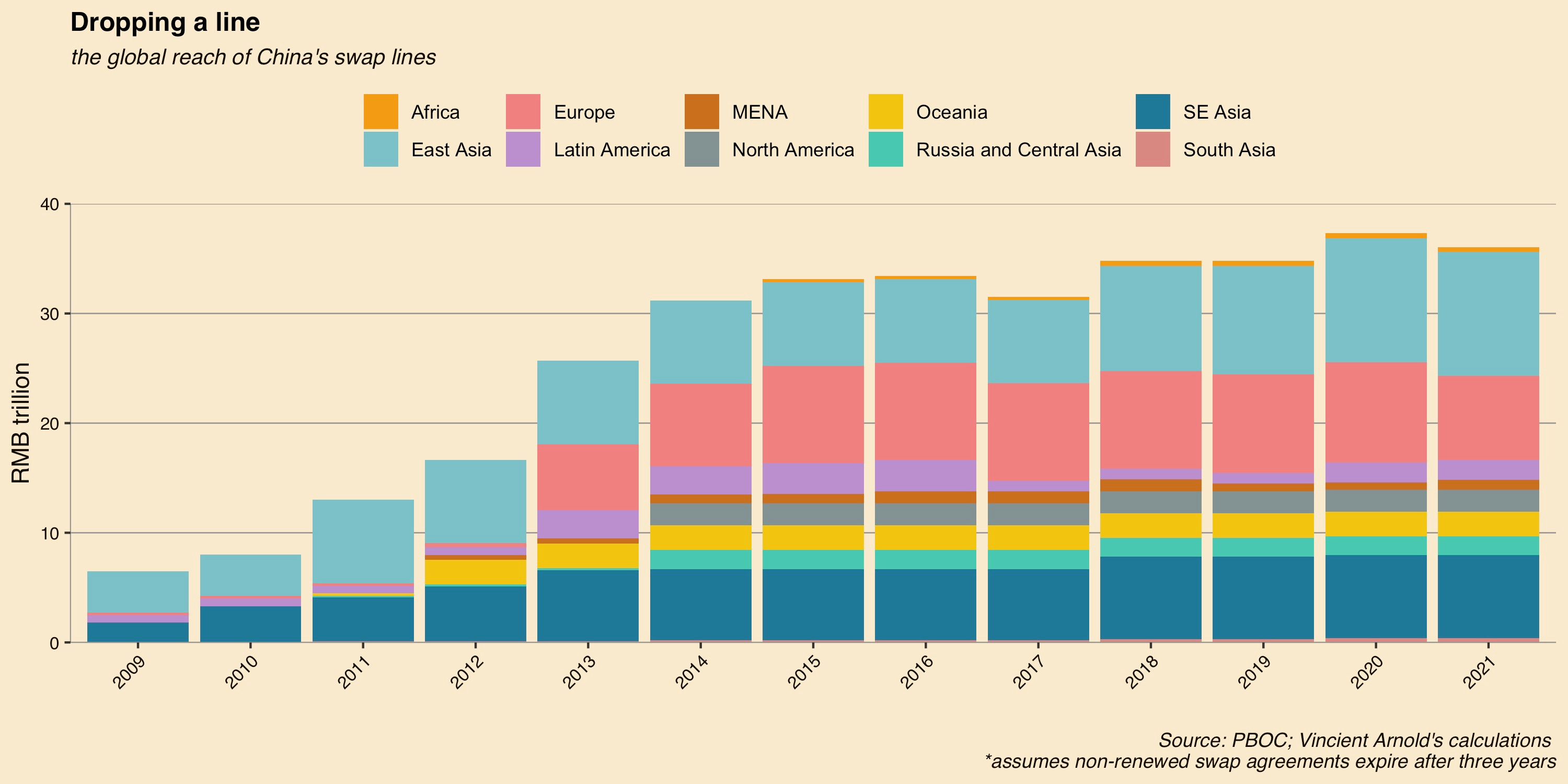

China though, has gone on a swap offensive. In the decade from 2010 to 2020 it expanded its swap network from seven central banks to thirty-one. To see the size of its swap lines by country over time, see this interactive web tool.

For comparison, in 2022, the US maintained standing facilities with only five. China has numerous reasons to do this: to internationalize the renminbi, lessen reliance on the dollar, and win influence abroad. On the whole, its swaps-driven renminbi internationalization efforts have been underwhelming, and they’re not the sanctions shield that they might appear. But China’s swap network does endow China with growing geopolitical leverage and influence as Beijing co-opts an ostensibly foreign exchange-oriented tool as an opaque catch-all lending instrument, becoming a de facto lender of last resort to nations around the globe.

What they aren’t: a renminbi internationalization silver bullet

Let’s start with some important context: China has significant capital controls. This means foreigners can’t just buy and sell renminbi-denominated assets in China at their will; the People’s Bank of China (PBOC) strictly limits conversion (and distinguishes by type: conversion for trade settlement vs. for investment). There are many reasons for its policies but at the heart of it, capital controls force domestic savings into state banks and therefore give the Chinese state the ability to allocate capital. At the same time that Beijing controls the convertibility of the renminbi, it wants the world to use it. This is where China’s swaps come in: Beijing can have its cake and eat it too (it reckons). China’s approach is, to itself at least, cogent—it believes that increased availability of the renminbi will beget international use of it. And, for many nations, the renminbi’s stability (it’s a managed exchange rate) means it’s an upgrade from local-currency financing. Swaps can grease the wheels, so the thinking goes.

In December of last year, President Xi unveiled plans to pay Gulf nations for oil and gas imports in renminbi, facilitated by central bank currency swaps, which would shelter China’s most critical imports from U.S. sanctions jurisdiction. Russia already sells oil to China in renminbi. If the Gulf nations agree to China’s plan, supported by the architecture of China’s vast swap network, it could amount to what economist Zoltan Pozsar calls “dusk for the petrodollar.” China’s swaps are covered most extensively by Beijing in its 2021 Renminbi Internationalization Report, the name of which sort of gives it away: the swaps have always been a tool to internationalize the Chinese currency.

But the story is more complicated.

Imagine you’re on a used car lot looking to purchase a car. As you walk past a sedan, a salesperson approaches you and says she can offer you an insurance deal on that specific car because she has a special deal with the manufacturer. Do you buy the car? I don’t know. It depends. All else equal, the provision of comparatively cheap insurance with broad coverage would, on the margin, make you more likely to buy the sedan. But not all else is equal: you’d have to want the car in the first place. Swaps lines are somewhat similar. They provide insurance against a liquidity shortage, making it easier and safer to transact in the currency and hold assets denominated in it. But again, you’d have to want to use that currency in the first place. Using the provision of insurance to enhance the desirability of the product is to put the cart in front of the horse.

The proof is in the pudding: according to SWIFT, following China’s decade-long swaps blitz, in 2021 the share of the world’s international transactions cleared in renminbi was an underwhelming 2.1 percent, compared with 0.6 percent in 2012. Its use as an international reserve currency has also been lackluster. By 2021, it had managed only 2.6 percent. For context, in 2021 China represented nearly one-fifth of the world’s economy when adjusted for purchasing power parity. Reductively, if the current relationship between the aggregate size of China’s swap network and its share of international (defined by SWIFT) payments were to hold, China’s swap network would need to balloon to 131.2 trillion yuan ($18.2 trillion) in order for its share of international payments to reach just 10%. That’s more than three times its maximum historical size and would represent a number just barely smaller than that of the entire Chinese economy (!).

The true drivers of global reserve status of a currency are complicated and hotly debated (especially of late, as the perennial “dollar death” discussion is back in vogue), but most scholars agree that crucial to the recipe are safe-asset status of currency-denominated debt (e.g., what Treasuries are to dollars), stability (i.e., non-volatile exchange rate), and liquidity (i.e., ability to exchange the currency at will at any time). Swap lines are an inferior substitute for those structural conditions. PBOC swap lines may grease the wheels of renminbi internationalization, but they are not the engine of its (sluggish) growth.

What they aren’t: an airtight sanctions shield

While reaching international reserve currency status is an “offensive” (putative) benefit of China’s swaps, it’s not necessary to play sanctions defense. China can de-dollarize/internationalize its own trade with the world and that would be enough to build a Fortress Beijing against sanctions. The critical piece here is that China doesn’t need the renminbi be to become a global reserve currency in order for it to shelter the nation from Western sanctions. It just needs to denominate bilateral trade with China in renminbi. China is a huge economy with plenty of domestic production (the “world’s workshop”) and a net exporter, so it doesn’t need to change that many imports to being renminbi-denominated to reach a higher degree of sanctions-insulation for its most crucial imports. The idea may sound far-fetched, but recall that Iran successfully received payments for oil exports in monetary gold while under American sanctions. If Iran—a much smaller and less globally significant economy—can avoid sanctions using gold, it’s not hard to imagine a world in which China successfully deploys its network of preexisting swap lines to expand renminbi-based bilateral trade during a Western sanctions standoff.

Daniel McDowell has documented the swap-sanctions relationship in a new book (I’m not affiliated, it’s just a great read). He shows that countries with moderate risk of US sanctions often look to swap lines for protection. After America’s first sanctions salvo against Russia for its invasion of Crimea in 2014, China announced an expansion of its swap line to Russia, which Russia tapped in 2015 and 2016. Indeed, McDowell analyzes data about sanctions exposure and swap lines and shows that there is a statistically significant relationship between sanctions risk and desire to obtain swap lines.

But there’s more to de-dollarization and sanctions than swap lines and, as McDowell points out, anti-dollar policies like swap lines often don’t work—interest in swaps and swaps successfully protecting you from sanctions are distinct issues. At their core, the strength of US (and, to a lesser extent European) sanctions rest on the centrality of correspondent banking relationships and payments systems. In other words, to use dollars, you’ve gotta have an account at the Fed, or bank with someone who has an account at the Fed, or bank with someone who banks with someone (and so on, you get it) who has an account at the Fed. That’s the magic behind the legal force of sanctions: US legal jurisdiction covers US entities and ultimately, if you have to clear payments through the New York Fed, you’re dealing with a US entity. This is a source of frequent misunderstanding: while sanctions are targeted at foreign institutions, they actually apply to American ones only. But the vast majority of payments go through the Clearing House Interbank Payments System (CHIPS), which is comprised of American institutions or foreign institutions with a US bank branch (and therefore still subject to US law). So, in other words, sanctions don’t target a central bank receiving a currency; they target companies’ abilities to send and receive that currency. For example, US sanctions blocking dollar payments would fail to work if a Bolivian citizen bought US cash bills at a money-exchanger in La Paz and then went across the border and used that cash to pay for goods or services in the streets of Peru. There’s no US company or natural person involved in the movement of that money, so the sanctions don’t help.

This is why swaps aren’t themselves a panacea. It’s possible that, for example, a Nigerian company wants to export oil to China and Beijing would like to activate its swap to avoid sanctions. Fine. So, the Central Bank of Nigeria could active the swap line, exchanging naira for renminbi. Also fine. The Nigerian oil-export company has renminbi to pay the Chinese importer and oil to give them. Now, though, you have to make a cross-border payment, and you’re probably stuck with correspondent banks that, ultimately, use CHIPS to clear that payment. So, the swap got you renminbi, but if there are US sanctions involved, you still can’t move it around, which, in the realm of paying for things is, you know, important. To be sure, there are second-order effects here; if banks in Nigeria know they’ll always have renminbi liquidity (because of the swap), they may start to invest in the infrastructure to clear non-dollar payments themselves and Nigeria and China, in this example, might start work on a bilateral clearing system (Russia and China did this, albeit to negligible effect).

In an admittedly simplistic analogy, if money is represented by bulk goods and payments are the shipping lanes on which those goods are moved, it’s fine to substitute American goods for Chinese ones, but you don’t really escape US dominance until you can replace both the goods and the ships carrying them. Swaps help with the goods, not so much the shipping. Revisiting the China-Russia swap line, it may then come as no surprise that the Carnegie Endowment has called the line “a damp squib.”

Geopolitical leverage and bailing out the Belt and Road

The real policy challenge posed by Chinese swaps to the West is a softer challenge, the contours of which only become clear in the aggregate. That challenge is geopolitical leverage and the swaps’ ability to endow Beijing with a sort of ersatz lender of last resort (LOLR) facility internationally.

Start with how swaps typically work. Let’s imagine a wild world in which there was international exposure to a financial pipe bomb like, I don’t know, US subprime mortgage-backed securities. Those would be dollar-denominated and in a crisis, dollar funding markets might seize up. So European banks might need dollars, and the European Central Bank (ECB) would draw on its swap line with the US, supplying short-term dollars to European banks until funding pressures alleviate. For a few months, when market funding exceeds the (comparative high) price of a central bank swap, European banks might rely on the swap line to temporarily alleviate a shortage of dollars in Europe. In such a world, swap lines are drawn on and the borrowing central bank then auctions off the resulting foreign exchange to its own domestic banks at the same rate as it is charged by the lending central bank.

Recent work by Sebastian Horn, Bradley Parks, Carmen Reinhart, and Christoph Trebesch has shown that the emerging Chinese model looks somewhat different. First, it’s very rare that there are genuine renminbi liquidity shortages abroad (though they do happen from time to time in offshore renminbi trading centers like Hong Kong and to a lesser extent in heavy China-bound exporters, like Mongolia). However, China’s realization was that just having the ability to hold renminbi against easy and cheap collateral (one’s own currency) might be, for certain countries, pretty attractive. In other words, in the absence of a liquidity shortage, a swap line could be deployed just like any other repo facility: it allows the borrowing central bank to borrow renminbi against collateral comprised of its own currency, ostensibly for a short period, but one that could, theoretically, be serially rolled. In this way, China can provide stable foreign currency reserves (for an often-hefty fee) to a borrower under the radar: it doesn’t look like a massive loan, and it benefits from the opacity of international central bank operations. Deployed like this, the swap line is really a conduit for rolling short-term financing of a country’s reserves: instead of the borrowing central bank auctioning off renminbi to resolve a shortage in its country, it could use the renminbi to intervene in currency markets, protect its dollar reserves for import payments, or even pay off IMF debt. It becomes a medium-term central bank bailout disguised as a short-term foreign exchange tool.

In fact, the paragon of this dynamic has recently played out in, of all places, Buenos Aires. I have written about this in depth in a nearby blog. In a watershed moment, Argentina drew on its PBOC swap line to pay off debts to the IMF, in essence replacing IMF debt with Chinese swap line debt. This is a crystallized example of Beijing’s efforts: it has deployed a foreign exchange crisis-intervention tool to serve as a stop-gap IMF alternative (that comes with a lot less press coverage and disclosure). Here’s a bit from the blog:

The recent move by Buenos Aires to utilize the short-term crisis-management tool (which the [Argentine central bank] itself classifies as 0–3-month debt) to finance much longer-term IMF debt marks a milestone in the extent to which nations have used central bank swap lines to finance fiscal debts.

Reliance on short-term lending to fund longer-term obligations is precarious at best. And this is key: swap lines are short-term funding, no matter what they may seem. Ask the people working repo desks during Bear Stearns week—just because you renew overnight debt every day for six months does not make it six-month debt; the second the lender decides to stop rolling, they pull the rug from under the borrower and the game is up. And that is plainly a source of leverage (of the geopolitical/suasion variety).

This wouldn’t be the first time China has stepped in to bail out a country with a plummeting currency either. In 2015, Mongolia owed China more from its swap line than it reported in its total foreign reserves at year-end, and used almost the entirety of the loaned renminbi to defend its tanking currency (which only softened the blow—it lost 105% in ten years). Chinese officials reportedly used Mongolia’s reliance on the swap line to extract political concessions, including about Mongolia’s stance on Tibet. The Mongolian national security council later issued a classified warning to the central bank.

But the swaps are a global effort and jigsaw neatly with China’s other flagship influence-building operation: the Belt and Road Initiative, a globe-trotting infrastructure funding program. Indeed, IMF research shows that nations with high levels of external debt and low foreign reserves are more likely to pursue a swap. Recent evidence points to China using its swap lines to bail out countries that became indebted by borrowing heavily from China in the first place. Laos, Turkey, and Sri Lanka all are reported to have used their lines to top up reserves. And the PBOC’s swap rates far exceed IMF standards. China is opportunistically loaning out foreign reserves to nations in fragile positions for hefty fees, often adding to a tab of unsustainable debt owed to Beijing.

The focus, though, isn’t always on developing nations and it’s easy to focus on the renminbi and miss the debt forest for the currency trees: China’s swaps are, in many ways, just another form of credit facility. In the case of South Korea, the nation hardly cared about the renminbi but China’s clout as a result of the swap line (it was one of South Korea’s largest standing liquidity facilities) led South Korean officials to worry about the nation’s financial security if it hosted American missile defense systems. In other words, renminbi aside, China’s swaps give it a new form of credit facility to extend to other nations with the blanket of confidentiality afforded to international central bank operations.

This doesn’t mean China’s going to call in its debts and seize the borrowing nation’s resources—central bank swaps have little recourse and the borrower can always print more money (though the ensuing inflation would hurt in many emerging markets). The point is that China’s swaps (and all swaps, for that matter) are structured as ‘mutual consent’ agreements: the borrowing country must request a draw and China must approve it; this structure gives China leverage in the transaction, especially during a crisis. Beijing has positioned itself as the lender of last resort via swaps for many emerging-market economies that may face a critical balance-of-payments problem. Instead of turning to the more transparent (albeit more interventionist and slower) IMF, they’re now more likely to borrow from China, and with even less transparency than via formal loans. The line between finance and statecraft is blurry and China’s swaps straddle that line.

The way forward: multilateralism, conservative repo, and a little perspective

While challenges to Western policy exist in China’ swaps network, Western policymakers are also prone to exaggerate the “China threat.” In the realm of renminbi internationalization, the swaps have been largely a flop. Doling out emergency liquidity lines for a currency few country want makes Chinese swap lines look like a hammer in search of a nail.

While the swaps might result in geopolitical leverage, that only occurs when they’re used—and most aren’t (see the swap line visualization tool). Plenty of central banks accept the swaps as a cheap diplomatic concession with little intent or need to use them (e.g., the ECB). And what’s the harm there? Having a contingent credit facility that one doesn’t need to use costs the recipient country next to nothing, but results almost instantaneously in a contingent credit facility and goodwill in Beijing. The line would only present a geopolitical risk when three conditions are met: (1) the country uses the swap line; (2) the country relies on that swap line and its renewability; and (3) the country has some geopolitical tension with Beijing. The main first-order risk of accepting a Chinese swap line you don’t really care about is just that maybe you’ll ruffle feathers in Washington. For a prospective recipient country, there are some obvious if limited tangible benefits, but few very and mostly conditional costs.

China’s swaps are also mostly non-recourse. If a nation defaults on a swap debt, it just prints more money or borrows it from the IMF, leaving China with worthless devalued foreign exchange—China is the main loser in that scenario. (China has historically worked with the IMF on its swap lines in fact, in Mongolia and Argentina, but in the latter case dropped the pretense that it would only lend if Argentina complied with its IMF arrangement.) This may explain its seemingly excessive interest rates: yes, swap rates are higher than the IMF’s, but China is also lending to very risky countries without conditionality and against often highly risky collateral. What may appear extortive may also be prudent risk-adjusted pricing. And China is not alone in this approach: while its swap rates are higher than US swaps or IMF loans, they’re hardly higher than similar US Treasury bailout loans to Latin America.

With respect to sanctions, China’s swaps are mostly a red herring: nascent payments systems and central bank digital currencies are the more likely risks to dollar payments than central bank swaps.

And, while opportunistic, China’s swaps are filling a gap: developing nations often need quick access to foreign currency liquidity and don’t have the credit or collateral to get swaps from developed countries (in a private conversation, an emerging-market central banker told me their country had tried to get dollar liquidity and was denied, leading the bank to consider China). But if any institution should be doing that lending, it’s the purpose-built IMF. It made a first step in the right direction with its Short-Term Liquidity Line, which provides a swap for Special Drawing Rights (SDRs)—a special kind of IMF-accepted money-like instrument—against local currencies. But its lack of use (Chile signed up but never drew on the facility) in comparison to China’s swaps points to fundamental weaknesses. First, it’s not available to higher-risk countries and second, it requires a significant amount of time and negotiation, things that nations in crisis don’t have a lot of.

Better examples include the Fed’s Foreign and International Monetary Authorities Repo facility (see case study here) and the ECB’s Eurosystem Repo Facility for Central Banks (see case study here). Both offer a broad-based window to which nations can apply, anonymously, to get dollar or euro funding against eligible Treasury or euro-denominated sovereign debt collateral, respectively. The issue remains that many developing economies don’t hold enough eligible collateral to get meaningful amounts of dollar or euro liquidity. With the appropriate safeguards (short tenor, high haircuts), the Fed and ECB could consider accepting a broader range of collateral (like SDRs), which would likely expand the list of eligible counterparties. They could do this through existing facilities or set up new ones. The ECB has also established standing bilateral repo lines in which it lends euro against euro-denominated sovereign debt collateral, and it established these lines before a crisis so they can be called on in short order. The US could consider setting up a similar network to reach more countries and guarantee them liquidity if and when needed. Again, they may need collateral flexibility, but the ECB has shown a willingness to negotiate.

Conclusions

On balance, it’s hard to know whether China’s swaps do more harm than good for borrowers, but even if China has the best of intentions, transparency breeds trust and opacity invites suspicion. If Beijing wants to clean up its “debt trap diplomacy” image—regardless of how accurate that depiction may be—disclosures would be a good start. For Western policymakers, China’s swaps do pose challenges, but they’re largely challenges of a soft-power nature and those challenges may be receding as China pulls back investment from the developing world (in fact, I’ve heard from China experts that China’s appetite for renminbi internationalization has petered out under Xi Jinping, who opposes the “financialization” of China’s economy). Meanwhile, the swaps have filled a gap that Western policymakers and multilateral lending institutions have thus far been unwilling to fill. To counter China’s influence in the developing world and to provide liquidity where it’s needed most, the West ought to consider expanding its swap and foreign-exchange repo facilities. It should also consider broadening access to them, using risk-management tools to fine-tune their approach. A more proactive Western strategy would counter Chinese influence, but it would also improve much-needed access to foreign currency liquidity that is badly needed in the developing world. To borrow one of Mr. Xi’s favorite phrases, that seems like a win-win scenario.

(Disclaimer: This work is independent from and not endorsed by the Yale Program on Financial Stability or Yale University; all views are my own.)

I refer throughout to “the West.” It’s a ham-fisted phrase I don’t like but for which I have no great alternative yet. I adopt the Paul Tucker definition of the term, to mean liberal democracies, many of which are indeed not geographically in the West (e.g., the Antipodes, Japan, South Korea). And indeed, the opposite is also true: simply being geographically in the West is neither sufficient nor necessary for being in my “the West” club (e.g., I wouldn’t consider Belarus, no matter how safely in Europe, to be a liberal democracy).