New Note Out: Stablecoins, FX Arbitrage, and Geopolitical Shocks

geopolitical risk-off events and stablecoin pegs

I have a new note out nearby: Stablecoins, Geopolitical Shocks, and Imperfect Arbitrage: A Case Study of Türkiye. If you are (1) really interested in stablecoins; (2) a finance nerd and like the concept of the limits of arbitrage; or (3) neither 1 nor 2 but are out of melatonin, I suggest reading the full paper. If you don’t like reading (fair enough), here’s the highlight reel:

Abstract:

On March 19, 2025, a key Turkish opposition political figure was unexpectedly arrested on what were presumed to be politically motivated charges. In response, the lira depreciated sharply. Meanwhile, Türkiye has a large and active dollar stablecoin market. Using a time series dataset of trade-frequency Tether vs. lira trading, I exploit this natural exogenous geopolitical risk-off event to investigate the response function of stablecoin traders active in Türkiye to this shock. I find that the shock is associated with a large (5.33% ) abnormal depreciation of the lira. Further, I show that the shock is associated with an abnormal widening of fiat-synthetic dollar parity deviation beyond that which is characteristic of standard constrained dealer intermediation. I conclude that this exogenous geopolitical shock had large but short-lived and differential effects on fiat and synthetic dollar-lira markets, suggesting potential dollar market segmentation.

Geopolitical this, geopolitical that—Why should we care?

If you, like me, are somewhat suspicious of annoyed by the term “geopolitical” getting thrown around as an all-purpose modifier these days, you might be healthily skeptical of “geopolitical shocks” and FX arbitrage. Let me sell you on why we should care about geopolitical shocks, and why we should care about using stablecoins specifically to analyze them:

Safe-Haven Status: If we care about the safe-haven role of the dollar, then we should see it show up during risk-off events. But, as discussed below, that’s actually tricky for a number of reasons, since often those risk-off events contain other non-risk reasons that there might be price action (e.g., changes in dollar interest rates). So, clean risk-off events are actually pretty crucial to understanding safe-haven characteristics. Those risk-off events need not be purely geopolitical in nature, but for reasons discussed below, it is uniquely convenient if they are as close to purely geopolitical as we can get, for empirical tidiness reasons.

Real “pure” geopolitical shocks are actually rare: As previewed above, the issue with many “exogenous shocks” is that actually a lot of exchange rate data—in a covered-interest parity sense—is endogenized in them. As an example, if, I don’t know, the US bombs Iran or something, and you have a major IRR–USD move, you cannot pinpoint that move as a result of only geopolitical shock sentiment, since it also comprises expectations about growth in Iran (massively negative) and about oil price and inflation forwards. In other words, a geopolitical risk-off sentiment is some (probably large) part of the decomposition, but certainly not all of it and we should be worried about interaction effects. If you can identify a shock that’s pretty clean, you then have a nice empirical setup for identifying how much FX movement is driven by risk sentiment and not fundamentals.

Stablecoins are useful high-frequency proxies for dollar trading: It is probably somewhat shocking to many, but we actually don’t have very good globally aggregated high-frequency fiat dollar trading data, in large part because most FX trading is done over-the-counter (OTC), so there isn’t one centralized data source. If you make some identifying assumptions (discussed more in the paper), then stablecoins solve this problem for you since the vast majority of stablecoin trades are done via centralized exchanges (CEXs).

FX shock goldmine: Erdogan

So, you want to find a geopolitical shock on exchange rates. Following the first rule of macro (four economies: emerging, advanced, Argentina, and Japan), the second commandment is that if you search for bizarre FX market shocks, you should look to Erdogan’s Türkiye. Conveniently, Türkiye is also a major user of dollar stablecoins; for some related thoughts on this, see previous posts:

Stablecoins and the Dollar System

I recently came across this Fed note (otherwise about CBDCs), which included the following:

Eurodollar Stablecoins, Bills, and Monetary-Fiscal Entanglement: Part II

To recap, in Part I we discussed the history of monetary-fiscal arrangements in the United States, from the free banking of the 19th century to the primary dealer infrastructure of today. We learned that in the past, financial plumbing innovations have unlocked new sources of latent demand

In this case, though, it’s better than just his mismanagement of the central bank, it’s downright political thuggery that saves the day (emphasis added here):

At 05:34:58 UTC (8:34:58 a.m. local time), the Associated Press (AP) broke a news story reporting the c. 7:30 a.m. (local) arrest of Istanbul mayor and opposition figure Ekrem Imamoglu, among a group of 100 people, on alleged corruption and terrorism charges, which the AP characterized as “a dramatic escalation in a crackdown on the opposition and dissenting voices in Turkey” (Guzel and Fraser, 2025). Following the arrest, government authorities closed roads and banned protests. Despite these clampdowns, thousands soon protested at what they called a coup attempt. Lawmakers inside parliament also protested, and eventually walked out, disrupting proceedings . . .

This particular shock has three characteristics making it an ideal candidate shock for an exogenous geopolitical event. First, it was truly unexpected. We see no suggestion of anticipation effects in the foreign exchange market or otherwise, and the media reporting itself makes clear that this event was a shock. Second, even if there were some background anticipation of such a geopolitical shock in Türkiye, the timing of this shock was certainly unanticipated, given that the event was by definition a secret dawn raid, known only to those orchestrating it ex ante. As we will see, for our purposes in such high-frequency data, even minutes make a considerable difference in the market, with newsflow being absorbed and priced in within hours. So, even if one could make the argument that some amount of geopolitical risk was anticipated, the randomized timing of the shock within a 24-hour window makes it exogenous to markets. Finally, the shock is free of the interest- and exchange-rate anticipation effects that so often plague geopolitical shocks and introduce endogeneity. While, for example, a military conflict in the Middle East may have geopolitical shock effects on the exchange rate, it almost certainly also has at least two other anticipation effects: (1) an oil shock; and (2) an expectation of a recession and associated policy rate changes (which naturally affect exchange rates via covered interest parity). In this setting, the arrest of Ekrem Imamoglu has no obvious first-order financial or economic implications whatsoever, and so represents a clean risk-off event narrowly associated with geopolitical risk alone.

As a researcher, you don’t often get luckier than a dawn raid. It has long been my dream to exploit a night op for financial knowledge purposes, so I will be retiring now.

Depreciation and the limits of arbitrage

So, what happened?

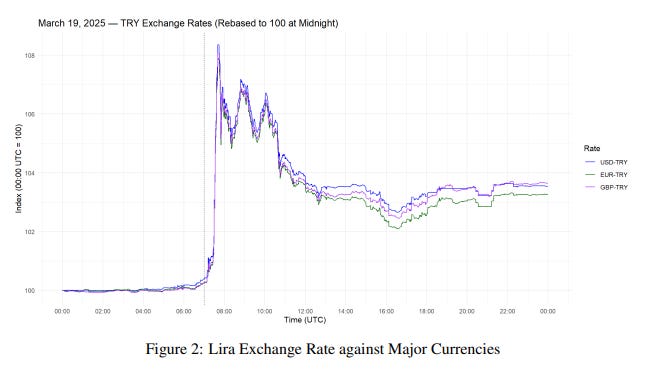

Lira-fiat currencies

First, let’s set the stablecoins aside for a minute and just look in an exploratory fashion at the fiat currencies:

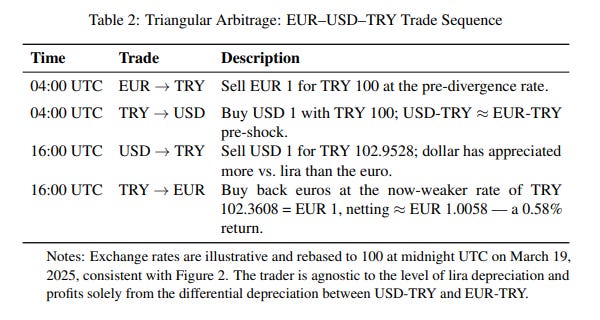

Gasp! Arbitrage!

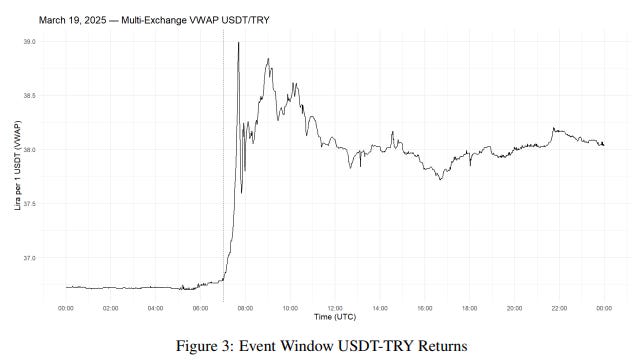

Lira-Tether

Now turning to stablecoins, the lira depreciated a ton against Tether (the dollar stablecoin of analysis in this case), which is not that shocking probably:

If you do a cumulative abnormal return (CAR) analysis, you find that the shock is pretty significant, driving a 5.33% depreciation of the lira against Tether in just two hours.

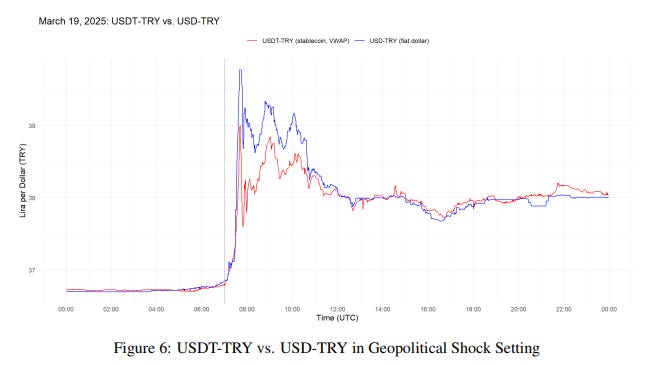

But that’s probably to be expected in direction if not in magnitude. So, the natural question is: did the fiat dollar depreciate the same way?

Lira-stablecoin vs. Lira-fiat (d.b.a. parity deviation or de-pegging)

Answer: not quite. Here’s a picture:

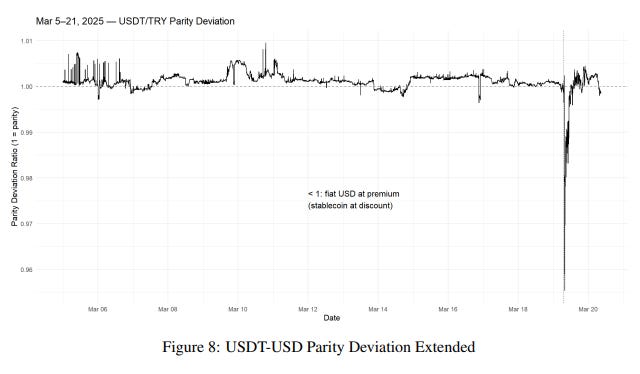

And we can redefine this along with the literature as “parity deviation,” where a value of 1 corresponds to perfect parity; a value of > 1 corresponds to a stablecoin premium; and a value of < 1 corresponds to a fiat premium. Here’s the picture, for the whole month of March (2025):

Gasp! Arbitrage again!

Parity deviation and balance sheet-constrained dealers

So here’s the thing about the scary picture above: we know from the literature that some of this parity deviation is to be expected as a result of balance sheet-constrained dealer firms (CEXs). In other words, it’s not all the shock, which is pretty obvious from looking at the chart: there’s persistent parity deviation between the fiat dollar and stablecoin dollar (read: $1 ≠ $1 in the lira setting) way before any shock.

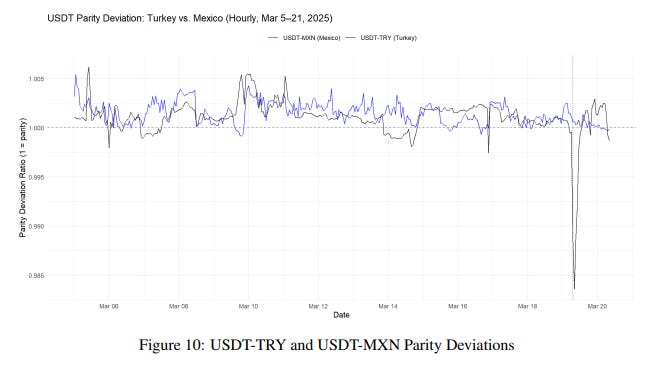

This poses an empirical challenge: we cannot naïvely show that the shock resulted in this parity blowout, because some of that deviation is already accounted for by the background noise of dealer constraints. To square this circle, we adopt the canonical diff-in-diff and use another EM currency (for which I had sufficient data), the Mexican peso, to show that the shock really did drive the wedge:

So, you arrested a political rival

You might have crashed your currency! I’d like to know how this played out when the coupsters in Niger locked up poor Bazoum in a basement, but the collective nature of the CFA Franc has deprived me of this opportunity. But, look, the upshot is that doing stuff like locking up political rivals actually might in fact matter, at least in the short-term, for markets (to be honest, I was suspicious that would be borne out cleanly in the data).

There are some other questions, namely as to where the missing arbitrageurs are (I assume they’re not actually missing, but that the opportunity isn’t there because of liquidity and fees).

The upshots I think are the following:

The lira depreciated considerably against other reserve currencies in response to a sharp exogenous geopolitical shock, and it did so differentially against the dollar relative to other currencies.

The lira depreciated against the fiat dollar and synthetic dollar (proxied by Tether), but it did so differentially in a statistically and economically meaningful matter.

Further, the breakdown in fiat-synthetic dollar parity was driven by the exogenous geopolitical shock and in such a magnitude that could be not explained by balance sheet-constrained dealers alone.

Different strokes for different folks

I personally interpret these outcomes in total as evidence to support a market segmentation hypothesis. The idea that the folks trading Tether are different than the folks trading the fiat dollar should seem pretty credible: We know that fiat FX trading happens on dealer desks in New York, London, and Singapore; stablecoin trading against the lira pretty much happens when the good people of Istanbul wake up and check their mobile accounts. In other words, fiat FX traders of any given FX pair tend to be more institutional and international; stablecoin traders of that same given FX pair are more likely to be retail traders living in the local-currency country. There are sophistication differences, information velocity differences, rational inattention, and time-zone factors that should make these two classes of trader structurally different.

That’s the theory at least. It’s not testable with the data I have here, so while I provide a factor model for this theory in the paper, it’s hard to prove statistically. The idea in the factor model, though, is that we’ll only really see this market segmentation factor in times of stress. If you’re inexplicably trading Tether-EM currency pairs somewhere and a war starts or something, DM me.

For more detail and charts, see the full write-up.