SDRs, the ECB, and the Nuance of Monetary Financing

an esoteric debate comes to the dev fin fore

We recently talked about Special Drawing Rights (SDRs)—what they are, how they work, and why they’re the subject of much debate. If you missed that primer piece, please check it out here.

In that piece, we noted that SDRs can be used for numerous things, some of them either implicitly or explicitly fiscal. I dropped a footnote about this, though, and noted we might revisit it:

Notably, one of these categories of things, per the table, is fiscal uses (whether to get on with normal government spending or to avoid new debt issuance). We may revisit this at some point because it’s kind of an interesting and under-appreciated angle: to some, this looks like monetary financing—creating money to get spent. This is indeed a controversial issue and a nuanced one, but poses real constraints on the creation and uses of SDRs.

Well, now we’re revisiting it. Cheers.

n.b.: Yes, this is an admittedly very in-the-weeds topic and perhaps a bit thorny, so I feel the need to justify this foray a bit: SDRs and their (lack of) use is an extremely important aspect of development finance, but moreover, this discussion opens a lot of interesting doors in discussing monetary financing, something that comes up a lot in the days of ~quantitative easing~. It is therefore very interesting, and a part of the political economy of central banking with which we concern ourselves from time to time. Bear with me.

An Unfortunate Definition

We know what SDRs are, and we’ll get to the relevant SDR recycling proposals shortly, but first we have to swallow the great monetary financing pill. This is an unfortunate definition (for me, the author) because it’s kind of a Pandora’s box that will, without much restraint and effort, turn into a labyrinthine discussion of quantitative easing (QE), Modern Monetary Theory (MMT), and the political economy of money-creation, all very interesting topics but topics that I’d very much like to avoid here.

So, in the name of brevity, we’ll define ‘monetary financing’ as the creation of central bank “money” (i.e., usually reserves—short-term/callable liabilities of the monetary authority) for fiscal purposes. Now, this definition might be a little broad (some would define it as “monetizing the fiscal debt,” or the creation of money to purchase one’s own government bonds) but for our purposes it captures the concept. Probably the easiest way to think of it is in the context of a politically captured central bank, often (but not always) in an emerging market, that buys up the government’s debt at whatever cost (interest rate) the government requests, therefore “monetizing the fiscal debt.” This often leads to inflation, defaults, and other ills. Another example is when a central bank is performing a responsibility of the fiscal authority, such as recapitalizing an insolvent bank (i.e., creating reserves and handing them over to an insolvent bank in exchange for shares). This is the type of thing that is often legally the responsibility of the fiscal authority.

Important Sidebar: QE and monetary financing—when the whole point is to alter the debt composition of the (consolidated) government

Now, without getting too deep into the QE/MMT debate, what I do think merits mention is that monetary financing is a much maligned and controversial term (you hear “the Fed is printing money to bail out the government” talk a lot), but when it comes to QE, it gets misappropriated and it’s often misleading at best or downright wrong at worst (indeed, QE is not legally monetary financing, as we’ll see).

Reminder: QE (quantitative easing) is when the central bank creates reserves to purchase usually long-duration government debt, with the aim of reducing long-term yields and therefore serving as an interest-rate cut for longer-duration debt markets. It’s aiming to do to the long-duration side of the yield curve the same thing that normal monetary policy does to the short-duration side of the yield curve. In other words, if the Fed, for example, wants to bring down overnight interest rates, it has standard monetary policy tools to do so, but if it wants to reduce 10-year interest rates, it may need to engage in QE.

Yes, the central bank is expanding its liabilities to buy up government debt, so it’s essentially “created money” to buy government assets. But from the fiscal authority’s perspective, its debt is de facto cancelled (it’s just owed to another part of the government). So, at the level of the consolidated balance sheet of the government (inclusive of both the fiscal and monetary authorities), its long-term government bonds essentially got wiped out (again, they’re just owned by another part of the government) and its debts to the banking system (which is all central bank reserves are) just got increased in the same amount. In other words, long-term fiscal authority debt just got replaced with the same amount of short-term monetary authority debt. So, vanilla-flavored government debt replacing strawberry-flavored government debt—who cares, it’s all government debt at the end of the day and we haven’t, on net, increased or decreased the quantity of it.

In other words, all that’s going on here is duration change: the consolidated government just basically shifted the term structure of its debt from longer to shorter. It’s not even really something a central bank has to be involved in. Theoretically, in the US, for example, the Treasury could issue $400 billion in short-term bills and use them to buy up $400 billion of its 10-year bonds. That’s in practice the same thing: you’re just replacing long-duration debt with short-duration debt. There’s nothing particularly special about the central bank doing it. [1]

The risk here, of course, is that (1) when you shift the duration of government debt way to the front end of the yield curve (i.e., make it super short-term), you might (but not always) create inflation, as you’ve shifted the net stock of wealth from being less liquid (i.e., less money-like) to being more liquid (more money-like); [2] (2) if the monetary authority is subservient to the fiscal authority, this might just be a route through which the government can rack up huge debts that the market would otherwise have disciplined it from issuing, allowing deficits to expand rapidly and, in extremis, also result in (hyper?)inflation.

Whew.

SDR, MDB, WTH?

As we covered in the primer piece, there are a number of proposals on the table for recycling SDRs, two of which we’ll discuss here. Resurfacing from the primer (footnote added):

World Bank SDR Bonds

Rich nations could buy SDR-denominated bonds issued by the World Bank, thereby swapping their SDRs for a bond that pays them interest and providing funding to the World Bank in the process.

This setup would preserve the reserve asset quality of SDRs—which is critical to maintain—while putting them to better use. They’d still get paid for their holdings (potentially exactly the same, if the bonds paid the SDRi rate), and they’re still reserve assets, but the SDRs get used.

The proceeds from these bonds would then fund the World Bank and allow it to do more critical lending, particularly if issued as subordinated debt, which would comprise capital for the World Bank, allowing it to stretch its balance sheet further.

This idea has been floated by Brad Setser and Stephen Paduano, see here.

SDRs for Hybrid Capital

Similar (but distinct) to the World Bank SDR bond proposal, the IMF recently approved a proposal to allow SDR holders to use SDRs to purchase hybrid capital in multilateral development banks.

Similar to the advantages of the World Bank bond proposal, such a framework could maintain the reserve asset qualities of SDRs, while putting the SDRs to much greater use.

For reasons we may explore elsewhere, this proposal is unlikely to go anywhere despite formal approval, which is interesting on its own merits. In short, the proposal is plagued by a network problem: it works if lots of countries participate, but fails to work when only a few countries sign up (an asset isn’t very liquid when only a few market participants trade in it —and remember, SDRs must remain liquid to preserve their reserve asset characteristics). [3]

Both of these proposals are in hot water, for sometimes similar and sometimes distinct reasons.

The first-order problem facing both proposals is fine and not all that interesting: not enough central banks have expressed interest in them and you really need a lot of central banks to agree (or at least a significant number of the biggest central banks) in order to guarantee sufficient liquidity. And recall that sufficient liquidity is critical, because any SDR asset needs to satisfy the conditions of being a reserve asset (liquidity being one of them). So, fine, your market isn’t deep and liquid enough to satisfy the liquidity requirements of a reserve SDR asset.

Okay, but like, why? I mean, why should anyone be so opposed to buying these things? The illiquidity issue is a self-fulfilling prophecy of course: if everyone agreed to buy the thing, it would be liquid, and ergo very buyable, and therefore very liquid, etc. So, what’s the issue with SDR bonds or hybrid capital? What, aside from the liquidity problem (self-created) is holding folks up from being willing to buy these SDR instruments?

I have been told in private conversations with people familiar with the deliberations (both from the World Bank and IMF side of things) that the issue is that the European Central Bank (ECB) (read: the Bundesbank) is concerned about these instruments on the basis of, you guessed it, ~monetary financing~ (and, in hybrid capital’s case, other ECB rules).

Let’s take hybrid capital first. The reasons for calling the central bank purchase of hybrid capital instruments monetary financing and/or off the table for other reasons are not too difficult to wrap one’s head around: namely, they’re de facto equity or, at a minimum, equity-like, instruments. This violates monetary financing prohibitions because providing equity funding [4] is something the fiscal authority does (we’ll return to this concept later); and it’s in violation of Eurosystem reserve management principles because . . . well, it’s a de facto equity instrument, which again, monetary financing concerns aside, Eurosystem central banks can’t buy for reserve-management. Fine. This isn’t an entirely novel restriction for monetary authorities, so it doesn’t take much imagination to get here.

But what about World Bank SDR bonds? Again, we can all get the first-order problem of illiquidity, but, again, we’re interested in the reason for that illiquidity: why won’t Eurosystem central banks buy these things? Well, here again, the villain appears to be monetary financing™.

Okay, but why?

On Teutonic Tenterhooks

So, I’m not really sure. No one seems really sure.

But Stephen Paduano, doyen of SDRs, has done some very serious thinking on this and has written about it extensively, namely in a piece titled “SDR Rechanneling and ECB Rules: Why rechanneling SDRs to Multilateral Development Banks is not always and everywhere monetary financing.” Perfect. With a debt of gratitude to Dr. Paduano, let’s explore the argument he makes for why SDR recycling via the purchase of World Bank SDR bonds (or, hybrid capital instruments, though that won’t be as much our focus here) should not be prohibited by Europe’s monetary financing rules.

First, he points out that not all SDRs are properly under the jurisdiction of the ECB anyways, in a technical carveout of the Eurosystem that allows national central banks [5] (NCBs) to do what they please with some of their assets. This is important because it frames SDR recycling activities as reserve management exercises, not monetary policy exercises (the ECB can still—and does still—sound the monetary financing alarm, but the bar is probably higher). The argument goes something like this:

Look, we get it, maybe you’re not buying SDR bonds for monetary policy operations, so we shouldn’t treat this that way.

That’s fine, but you can totally invest your reserves in many different ways—you buy gold, sovereign debt, and World Bank bonds (in all sorts of currencies) with your reserves, so why shouldn’t you be able to buy an SDR bond from the World Bank?

Also, look, the VTA market just isn’t that liquid, but in general World Bank bonds are, so wouldn’t you rather get your naked SDRs off your balance sheet and into some vehicle that’s more liquid? It would be in your own self-interest to shift your SDRs into a more liquid asset class regardless. [6]

Now again, this doesn’t mean that monetary financing rules don’t apply, but it reframes the issue as a reserve-management policy, which might matter insofar as NCBs get a little more leeway from the ECB on their reserves management than the Eurosystem gets on monetary policy.

Second, he points out that, as a result of a ruling of the Court of Justice of the European Union (ECJ), Eurosystem members can already buy SDR-denominated bonds. This is down to the QE issue. For those familiar, the ECB has engaged, like the Fed and Bank of Japan before it, in QE. To do this, it created reserves to buy up bonds. The ECJ ruled (wisely) that QE ≠ monetary financing (see earlier discussion of why), and as a result, the Eurosystem central banks already own lots of supranational debt.

Third, he argues that the ECB already implicitly allows rechanneling of SDRs to MDBs, and certainly allows central bank financing of MDBs: the European Investment Bank (EIB, a homegrown MDB) has access to the ECB’s liquidity facilities and can repo assets overnight at the ECB. And if it can do that, that should pretty well quell their concerns about the liquidity of any SDR instrument, right? Now, to be sure, we don’t know that the EIB has successfully repo financed any SDR assets, but that’s conceptually beside the point: the ECB is totally fine providing financing to MDBs, which appears to be the sticking point in the SDR debate.

Here’s Paduano (same piece, p. 10):

If a financing arrangement of any sort between the ECB, an NCB, and the EIB is viable, then rechanneling SDRs to MDBs should be viable. Put in negative terms, if the ECB and NCBs cannot rechannel SDRs to MDBs due to the prohibition on monetary financing, then the ECB is in violation of its own rules by establishing a funding arrangement with the EIB.

(!!)

Furthermore, the ECB has exempted IMF trusts (like the RST and PRGT, other avenues of SDR recycling discussed in the primer note) from the prohibition on monetary financing. Interestingly, though, it hasn’t done the same for MDBs. Here’s Paduano (p. 11, my emphasis):

Does [regulation EC3603/93] constrain monetary financing exemptions to the IMF, or does it provide the IMF as just one example of something which may be exempt? There is no EU treaty, EC regulation, or ECB ruling that would indicate an answer one way or the other. One prevailing “hunch” is that the IMF gets exempted while MDBs do not because the IMF performs essentially monetary operations, while MDBs perform essentially fiscal operations. If this is the case, it is a weak case. First and foremost, whatever the “fiscal” or “monetary” nature of MDBs may be, MDBs are not governments. Financing them is not “monetary financing” for an even stronger reason than that quantitative easing was not “monetary financing”: no conventional definition of monetary financing — the financing of the government by its central bank — is being breached.

I am more circumspect here (on the point of a “conventional definition”), a point we’ll come back to later.

Regardless of the interpretation of the specific EC regulation that exempts the IMF from such rechanneling efforts, it’s clear from public comments of ECB officials that this regulation isn’t really the binding constraint: rather, it’s the reserve asset characteristics and monetary financing concerns.

Let’s set aside, for a moment, the reserve asset characteristics bit and focus on the monetary financing concerns, not because reserve asset characteristics concerns are illegitimate, but because (1) they are somewhat endogenous to the monetary financing concern (if SDR instruments are not monetary financing, then they’re more liquid, and therefore more easily satisfy the conditions of a reserve asset); and (2) they may be a more serious concern about hybrid capital (on account of its equity qualities, as discussed), but should be much less binding for World Bank SDR bonds, which the ECB still appears to have issues with. Stephen Paduano and Théo Maret have already made the case for clearly reserve-asset eligible SDR bonds; the reserve asset characteristics aren’t the binding constraint here—it’s the monetary financing concern.

So, where are we on that? Let’s recap:

The ECB can clearly finance MDBs (e.g., its own financing of the European Investment Bank);

the ECB can clearly buy the debt of supranational entities and/or fiscal authorities (e.g., its Public Sector Purchase Program in QE);

the ECB has already made an explicit monetary financing carve-out for the rechanneling of SDRs to the IMF (though not MDBs).

And yet, the ECB still seems to have issues with SDR instruments on the basis of, you guessed it, monetary financing™.

Everything Everywhere as Monetary Financing?

Maybe the ECB is just being internally inconsistent, and hasn’t itself decided what exactly monetary financing is. Or, maybe, it takes a broader view of monetary financing. Recall that Dr. Paduano defined monetary financing (see quote above) as “the financing of the government by its central bank.” But recall that your humble correspondent defined it (see quote more above) as “the creation of central bank ‘money’ . . . for fiscal purposes.” My definition is a lot broader than his. I have a hunch that the ECB’s definition may be closer to mine. Let’s take a look. Here’s the Maastricht Treaty, article 123(1) (emphasis mine):

Overdraft facilities or any other type of credit facility with the European Central Bank or with the central banks of the Member States (hereinafter referred to as “national central banks”) in favour of Union institutions, bodies, offices or agencies, central governments, regional, local or other public authorities, other bodies governed by public law, or public undertakings of Member States shall be prohibited, as shall the purchase directly from them by the European Central Bank or national central banks of debt instruments.

It’s the emphasized bit that gets you here I think. Basically, Maastricht article 123 prohibits two things: (1) the creation of central bank reserves to purchase public-sector debt; and, crucially, (2) the creation of central bank reserves to do public (i.e., fiscal) undertakings (i.e., stuff). Article 123 is extremely broad. I am not a legal scholar and don’t pretend to be, but I’ve seen the second half of article 123 invoked before . . .

In the world of financial crises, central bank lending to an insolvent institution (or at least one known ex ante to be insolvent) is considered restructuring aid. That is, under EU law, a public undertaking, i.e., a fiscal authority responsibility. Back in 2009 when the Banco de España lent to Caja Castilla La Mancha, it knew that the bank was insolvent (though it didn’t say so at the time, resulting in much drama). In order to avoid breaking EU law on monetary financing, the Spanish treasury guaranteed that lending. This is important: a Eurosystem central bank was at risk of monetary financing by lending to a non-government body because it was partaking in a public undertaking, i.e., a fiscal authority responsibility. In other words, Brussels’ view on monetary financing goes well beyond simply financing one’s government directly—it applies to a central bank doing anything that could be considered fiscal. This is, of course, problematically broad and, given the ECJ’s decision on QE, already having its wings clipped.

But to be devil’s advocate: First, one could pretty easily define SDRs as central bank reserves of the ECB, on two levels: (1) they are, in fact, reserves held at central banks; and (2) by definition, for the ECB, SDRs do represent contingent claims on euro liquidity—i.e., a contingent liability of the ECB. Second, while the IMF is clearly a more “monetary” body (complaints about climate lending via the RST notwithstanding), resulting in its carve-out, it is not obvious that MDBs are. MDBs do fundamentally fiscal things, like lend money to governments to build schools and roads, etc. One could pretty easily get to, “we’re not cool with you guys using Eurosystem reserves, (contingent) claims on ECB liquidity no less, to finance port-building in Mozambique—that is just nowhere close to being a monetary operation.”

Fine. If we take that view on the merits, then we can see how the ECB might get there. But here’s the problem: SDR allocations themselves kind of risk breaching these rules, loosely defined as they appear to be. Let’s revisit, once again, the footnote I mentioned at the beginning here, from the primer piece:

Notably, one of these categories of [uses of SDRs], per the table, is fiscal uses (whether to get on with normal government spending or to avoid new debt issuance). We may revisit this at some point because it’s kind of an interesting and under-appreciated angle: to some, this looks like monetary financing—creating money to get spent.

Also from the primer piece:

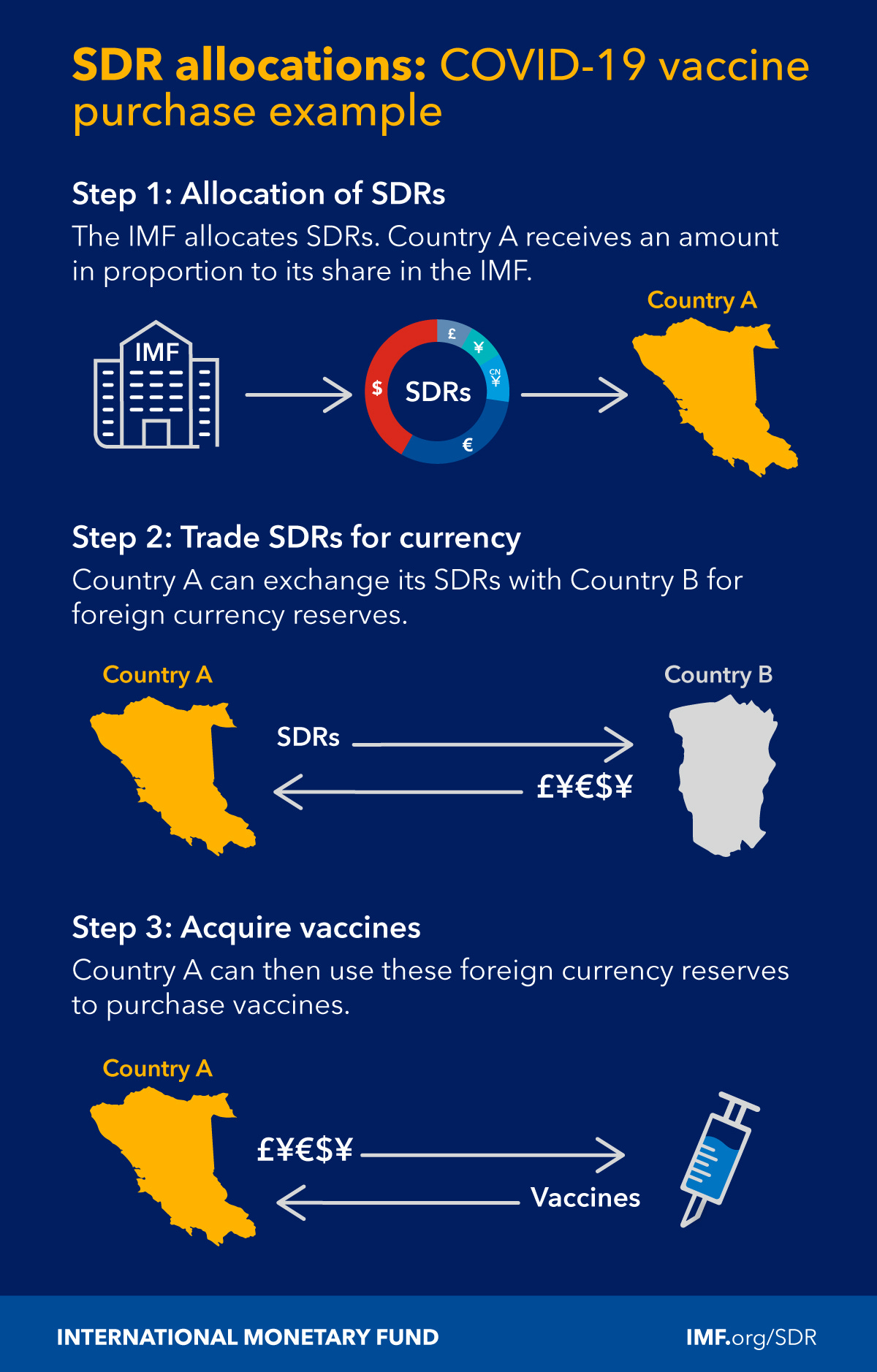

So, that’s, like, as fiscal as it gets? Let’s walk through this example again:

The Eurozone, among others, votes in favor of the creation of new SDRs, thereby creating contingent claims from the rest of the world on euro liquidity via the ECB.

As predicted and agree ex ante, some nation says, “ya know what, I’d like some euros for my SDRs, so that I can go do fiscal things.”

The ECB says, “sure, yeah, of course, that was the point of these things anyways,” summarily provides euro liquidity, and then points said nation in the direction of BioNTech.

Said nation is down some amount of SDRs and up the same number of euros. It thanks the ECB. It then proceeds to do fiscal stuff, like buy vaccines.

Everyone goes home happy (and, hopefully, vaccinated).

Sound like the EU’s definition of monetary financing?

But wait, that’s just the on-the-nose version. What if the padded reserves from the SDR allocation result in a recipient nation being able to avoid issuing fiscal debt? That appears to have been the case for numerous nations during the COVID crisis. Is that monetary financing?

Now, someone might interject here and say, “this doesn’t count, though; you’re conflating the creation of euro central bank reserves for euro area fiscal authorities with the creation of euro central bank reserves for other fiscal authorities.” First of all, I’m not sure that matters—I doubt the ECB would be cool doing a swap line with a country that was going to on-lend its euro liquidity to a construction company or to wipe out household debt. But let’s assume it does matter. Then that’s even more reason to not care about recycling SDRs to MDBs, which lend almost exclusively in not-the-euro-area.

And with That Extremely Unsatisfying Note, It’s Time to Close

I think we’re left with more questions than answers here, chief among them, “What actually is the ECB’s view of monetary financing?” If you are an ECB lawyer reading this, please do email me; I’m interested to learn more about this.

It’s an important question. Drawing bright lines between the monetary and the fiscal is always difficult (QE as exhibit A, not just in the Eurozone, but everywhere). It’s more difficult when the international angle appears. It’s twice that difficult when we start talking about SDRs. To be sure, I’m not a monetary financing nihilist or MMT apologist—monetary financing is a thing, and it’s an important thing to define, because there are real risks in true, irresponsible monetary financing. At the same time, though, clearly there is a fair bit of navel-gazing in trying to sort out what it is. The intellectual question, intriguing though it is, shouldn’t stop us from allowing pre-existing reserve assets from being used in the ways they’re intended to be used. This is especially true when it looks like there’s will (from France and Spain, for example) and legal precedent.

I will close by suggesting that this isn’t a uniquely European question. Particularly as it concerns SDRs, there are other currency-issuers (the US, UK, Japan, and China) that may one day have to wrestle with this question (even if it’s not currently their binding constraint).

Brussels, you have the con. *intensely American salute*

If you enjoyed this piece, please consider subscribing to receive updates and support my work.

I am grateful to Steven Kelly and Stephen Paduano for their valuable comments.

You can follow me on Twitter (X) @ArnoldVincient, or connect with me on LinkedIn.

This work is independent from and not endorsed by the Yale Program on Financial Stability or Yale University; all views are my own.

[1] Indeed, recent academic discourse on the Treasury market has pointed out that when the US Treasury shifts the composition of its debt toward the front end of the yield curve—in other words, toward short-term bills—its effects are very similar to traditional central bank QE.

[2] But it should be pointed out that plenty of very big economies have done QE at massive scales and not induced inflation at all (sometimes liquidity doesn’t jumpstart the economy like you want it to—sigh).

[3] For those unfamiliar with hybrid capital: We tend to think of a company’s “capital” as its equity. That’s usually right. But in some cases, particularly with banks, the regulatory system (“capital” is a regulatory construct) considers some non-equity instruments to be basically equity (hence the term “hybrid”). An example: a bond that, when a bank faces severe troubles, it can just wipe out (a.k.a., “contingent convertible” bonds, or CoCos *cough cough, Credit Suisse*). Many banks have “long-term subordinated debt” as some class (albeit not the best class) of capital. Fine. So, development banks need more capital. Why? Because they’ve got important stuff to handle: land wars in Europe (again), mass poverty and childhood malnourishment, a climate that increasingly feels like an oven, ISIS is in Mali, there’s a horror movie about Winnie-the-Pooh, and other lists of nasty sad things that would be on the warning label of life on earth. It’s all very dreadful. As a result, many multilateral development banks (MDBs) would very much like to sell some hybrid capital instruments to willing buyers to support their missions against war, famine, and other unsavory things.

[4] Of course, this gives rise to the “what even is equity” question, which, to be sure, like many things, is more a continuum than a discrete category. One could argue that debt—even of the most subordinated variety—is debt and not equity. But this would be to miss the point: the concept is that anything that’s very junior in the capital stack exposes the investor to risk, risk that monetary authorities are not often authorized to be taking because of legal systems crafted around the political economy and ethics of independent central banks. We’re generally okay with central banks buying (super safe) bonds to carry out price-stability mandates, but buying shares of Home Depot would be to walk off the farm: it’s not in the spirit of—or mandate of—a central bank to be taking ownership of companies.

[5] Brussels jargon is impenetrable. The Eurosystem is comprised of the ECB and the NCBs (Bundesbank, Banque de France, Banco de España, etc.). They all form the Eurosystem that carries out ECB directives.

[6] The idea here is that an SDR-denominated (but potentially hard currency-settled) bond would be more liquid than plain SDRs. This is, deductively at least, pretty cogent, given that the market for World Bank bonds tends to be much larger and more liquid than the market for SDR-to-hard currency trades (which, by definition, are only done between prescribed holders and mostly via the IMF).