Argentina, the US, China, and Swap Lines

a brief history and overview

As frequent fliers know by now, the geopolitics of swap lines is a favorite topic here, and while I don’t currently have the bandwidth to do a huge deep dive into the ongoing US assistance package to Argentina, I want to at least provide some background context, which should give you the quick-and-dirty on navigating the headlines. In Q&A form:

What are swap lines?

Literally, what are they?

Swap lines are arrangements—usually (but not always!) between central banks—to exchange one currency for another at some initiation date and then swap them back at a pre-agreed exchange rate in the future. One way to think of them is that they are repurchase agreements (repos) collateralized by foreign currency.1

I wrote a standalone primer on central bank swaps lines, which I’d encourage readers to check out. Additionally, some more comprehensive coverage can be found at the Fed and the Yale Program on Financial Stability.

Why do we have them?

Nine times out of ten, swap lines are extended because of funding pressures, i.e., spikes in borrowing costs in offshore currency markets. In practice, this means that it gets really difficult/expensive for European or Asian banks to borrow dollars, so to calm those dollar funding stresses, their monetary authorities obtain a swap line with the Fed. This is the answer you’re most likely to get from a central banker, and they’ll tell you about the cross-currency basis swap spreads (the cost of borrowing dollars abroad) rising sharply. This is true not just of the US, but to a lesser degree also for the ECB and their euro swap lines.

In reality, there can be other reasons at play too, although they’re much less common. For example, you might draw on a swap line to obtain large amounts of foreign currency so you can lend to a specific bank that’s on the brink of failure and has lots of foreign currency-denominated liabilities (and/or assets), as Iceland and Switzerland have done. In the context of emerging market economies, you might extend swap lines to help support another country’s currency, as the UAE has done for Türkiye, or as China has done for Argentina; or to try to internationalize your currency (or for other geopolitical means), as China has done.

What’s this ESF/Treasury stuff then?

Are Treasury swaps a thing?

Yep. Earlier I said that swaps are usually but not always between central banks. That is true, because historically fiscal authorities have also done swap arrangements. In fact, in the 1930s, US dollar swaps were extended by the Treasury through the Exchange Stabilization Fund (ESF), not the Fed (although this changed in coming decades). The ESF is a pot of Treasury money2 composed of foreign exchange (technically, foreign exchange, gold, and SDRs) that is held in a segregated account at the New York Fed (segregated from the Treasury General Account, that is). In more recent history, the Treasury has used the ESF to provide swap lines other countries, namely in the 1982 and 1994 Mexican crises. Historically, the use of the ESF, whether via swap or spot transactions, was mostly to do with the exchange rate of the dollar and/or other currencies (and prior to 1971, to gold). But the Treasury has also used it extensively in credit operations to support various countries. (Fun fact: the first use of an ESF credit loan—a few were offered but not used before then—was to Mexico in 1938 for $10 million.)

Intervening to affect the level of the exchange rate—or to aid other countries’ fiscal positions—is a fiscal policy decision in the US, and ergo a Treasury consideration, in contrast to standing or broad-based dollar swap lines extended by the Fed, which are for monetary policy and financial stability purposes. That said, it bears noting that the New York Fed is the fiscal agent of the Treasury (i.e., the Treasury’s bank) so any transactions done out of the ESF are staffed and executed by members of the New York Fed’s Open Market Trading Desk.

Does this make the swaps different?

Definitely. For one, as mentioned above, they are inherently political tools when housed in the Treasury. This also has ramifications for the their use; while Fed swap lines are authorized under Section 14 of the Federal Reserve Act (authorizing open market operations) and approved by the Fed’s Board of Governors, Treasury swap lines from the ESF are authorized by executive authority (via the Secretary of the Treasury with approval from the President). Authorizing legislation for the ESF is the Gold Reserve Act of 1934 (as amended) and Section 7 of the Bretton Woods Agreements Act of 1945 (as amended).

The other obvious difference here is that the Treasury is not the monetary authority and therefore cannot create reserves (and the pot of money is the ESF, a segregated account, not the Treasury General Account in any case). This means the lending is inherently limited. For reference, Mexico’s NAFA swap line with the Treasury is $9 billion; the total size of the ESF3 is $219 billion (of which about $16 billion is harder-to-liquidate assets and SPV investments); and the largest amounts outstanding drawn under a Fed swap line from a single counterparty was over $300 billion (from the ECB during COVID).

There are also reporting requirements on longer duration loans,4 but the 1995 precedent (as well as earlier 1982) with Mexico shows this isn’t a crazy hurdle. I won’t spend too much time on it here, but it’s worth noting that there were some legal controversies in 1995 regarding the term of ESF swaps. This prompted a memorandum from the Attorney General’s office to the Treasury Department on the use of the ESF for long-term (up to five years) swaps confirming the Treasury’s interpretation of the relevant statutes. Of interest is the use of the language “unique and exigent circumstances” which somewhat mirrors the language of the Fed’s Section 13(3) authorities (“unusual and exigent circumstances”). All to say, while there was initially some thought to restricting ESF loans to shorter durations,5 that view was put to bed in the summary memorandum, if not before then in 1982. It is well codified today that the Treasury can lend for long durations via ESF swaps.

In short, the main differences vis-à-vis Fed swaps: (1) governance; (2) purpose; (3) scope/scale.

What’s going on with the US and Argentina right now?

I’ll let Sec. Bessent himself tell you:

The [US Treasury] stands ready to purchase Argentina’s USD bonds and will do so as conditions warrant. We are also prepared to deliver significant stand-by credit via the Exchange Stabilization Fund, and we have been in active discussions with President Milei’s team to do so.

The Treasury is currently in negotiations with Argentine officials for a $20 billion swap line with the Central Bank. We are working in close coordination with the Argentine government to prevent excessive volatility.

In addition, the United States stands ready to purchase secondary or primary government debt and we are working with the Argentine government to end the tax holiday for commodity producers converting foreign exchange.

So, there are really three things going on here: (1) a swap line; (2) potential bond-buying; (3) ending a tax holiday for commodity producers. The purposes of (1) and (2) are the same as in the past: to support the peso and Argentine government debt (which kind of go hand-in-hand). The tax holiday issue is new to me, but also seems to be targeting pressure on the exchange rate.

What prompted the support?

In short, a run on the peso (for the 1,000,000,000,000,000th time)—nothing new under the sun here. To hear Bloomberg put it: “Javier Milei has lost the confidence of investors and he knows it” (!). To hear Mr. Milei put it, “the market is in panic mode.” In just three days last week, the Banco Central de la República Argentina (BCRA) intervened with over $1.1 billion (at a time when markets estimated reserves stood at <$20 billion).

The current situation is pretty standard of this sort of EM currency crisis: markets think the peso is overvalued and want the BCRA to let it float, and fear that they won’t be able to defend the peg. Mr. Milei and the BCRA would like to tame the volatility. This is well-trodden ground for emerging markets, and often ends in tears, without overwhelming intervention force. Context here is important, too: Argentina has had episodic balance of payments crises with such frequency that it has become the punchline in many traders’ jokes. In other words, the shadow of crises past looms large over Buenos Aires.

What might the swap line to Argentina look like?

Good question; not really sure. ESF swaps are done on an ad hoc basis. What we know thus far is that it was announced at $20 billion, and we know that swap lines from the Treasury in the past have come from the ESF.

For some historic context, the peak amount announced for Mexico for its 1995 swap was $20 billion,6 which was roughly 5.3% of Mexican GDP at that time. Today’s announcement of $20 billion would put the swap at roughly 3.2% of Argentine GDP, so well within historical bounds.

Notably, Argentine reporting suggests that a condition of the $20 billion swap will be to use $5 billion to extinguish the swap with China (see more on China below).

What about the bond-buying scheme?

Direct purchases of sovereign debt to support Argentina would be a strong direct intervention, and to my knowledge the ESF has mostly used stand-by credit or guarantees, rather than direct bond purchases. Those do have similar effects, though. For example, in the 1995 intervention, the US government included in its aid package an agreement to guarantee Mexican sovereign debt, which would have the same result of lowering yields (via the risk premium channel rather than the demand/supply channel). Notably, Mexico did pay a premium for that insurance, and there were preconditions.

Where does the IMF come in?

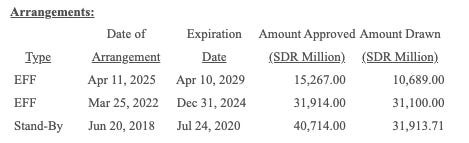

The IMF is the ultimate sovereign lender of last resort, to which Argentina is a frequent patron. (As of April, loans to Argentina, which represents <0.6% of global GDP, represented 34% of the IMF’s loan book.) Currently, Argentina benefits from numerous arrangements with the IMF:

Most recently, Argentina obtained—with strong US backing—a $20 billion EFF package. Now, notably, the IMF and US Treasury are not competitors here, rather collaborators (at least ideally). The statutory language related to ESF use is pretty clear that it should be used, “consistent with the obligations of the Government in the International Monetary Fund on orderly exchange arrangements and a stable system of exchange rates” (31 U.S.C. § 5302(b); my emphasis).

It was overshadowed by the Bessent/Trump announcement, but Milei also met today with Kristalina Georgieva.

How are markets reacting?

Well. It’s pretty soon (and light on details) to tell, but immediate signs are positive, which is no surprise. Reuters provides a nice smattering of economists’ notes, which I would characterize roughly as, ‘this is a material show of strength and lops off the left tail in the short run, but we’ll have to see how structural weaknesses are handled in the medium and long term.’

Is there politics at play?

Well, yes. I mean, there are geopolitics at play insofar as any Treasury swap line (some might argue any swap line) extension is an inherently geopolitical decision to some degree (in fact, Sec. Bessent explicitly said the package was symbol of the “geopolitical strategic importance of the relationship between the United States and Argentina”). There are also some more partisan politics at play;7 Argentina’s president, Javier Milei, is facing midterm elections next month after having suffered a brutal defeat in provincial elections a couple of weeks ago. Mr. Milei is an outspoken ideological ally of President Trump.8 Again, there is precedent here: the US pushed against IMF board concerns to approve a $20 billion IMF package in April (when the potential of a US credit line was first mentioned by Mr. Bessent).

Why is China relevant?

China’s current central bank swap line with Argentina is $18 billion, and its swap line at one point represented nearly 95% of Argentine reserves. In the past, it’s been used to support the peso by “putting money in the window” of the BCRA. I have written about this somewhat extensively, here and here. China’s recent (past ten years) history with Argentina has been significant, viewed as savior-like or with alarm, depending on whom you ask. I surmise from private conversations that Argentina turned to China in the past for wont of more forthright American support, and we’ve talked on this site about how China’s swap lines have been used as a geopolitical tool as much as a financial fire extinguisher. China has even used its swap line as a bridge loan to an IMF package for Argentina.

Taken together, the IMF and China have provided a huge chunk of the BCRA’s reserves in recent years. In fact, as Brad Setser points out, if you strip out reserves from the IMF and the People’s Bank of China, Argentina’s reserves position has looked worse throughout 2025, not better.

Which perhaps begs the question: agnostic to who’s in the White House, is this latest announcement good diplomacy on the side of the US? Probably. I have urged before that the US should be more active in its financial diplomacy, and in particular with this type of situation. That being said, it’s hard to be agnostic to who’s in the White House, and it’s unclear to me how much of this is about aiding Argentina or aiding a fellow right-wing populist politician in Latin America. Time might tell in the end.

Was this helpful? Further questions? Drop me a line at vincient.arnold@yale.edu.

Technically there are legal differences vis-à-vis repos insofar as swaps are arranged as back-to-back spot transactions instead of repurchase agreements, where collateral custody would change hands.

It was originally capitalized by the 1934 gold devaluation. Its reserves are managed by a team at the Federal Reserve Bank of New York on behalf of the Treasury.

As of July 2025.

The statutory language: “a loan or credit to a foreign entity or government of a foreign country may be made for more than 6 months in any 12-month period only if the President gives Congress a written statement that unique or emergency circumstances require the loan or credit be for more than 6 months” (31 U.S.C. § 5302(b)).

The language: "We find it telling that when Congress was considering what eventually became the 1977 amendment to section 10(a) of the Gold Reserve Act, it apparently gave some thought to restricting use of the ESF to short-term lending exclusively so that the ESF would not compete with the IMF— which was seen as the primary vehicle for longer-term lending. In fact, a question to that effect was posed to a Treasury Department official during the course of a Senate Banking Committee hearing that explored, among other things, the relationship between lending under the ESF and lending under the IMF.” (footnotes omitted)

Though the total aid package was worth $48.8 billion.

Elizabeth Warren has weighed in, in opposition, for what that’s worth.