Euro Emergency Liquidity Then and Now

a step toward euro internationalization?

International LOLRs

Readers will be familiar with the concept of central banks acting as international lender of last resort (LOLR), providing their currency to foreign monetary authorities when in need. The story of post-World War II financial history has been mostly about Federal Reserve swap lines, given the dollar’s status as the world’s international reserve currency. However, there is a second reserve currency, often underappreciated, the euro. And there is also another form of foreign currency LOLR—foreign currency-denominated repurchase agreements (repo).

We’ve talked about this nearby, but essentially a swap line is when central bank A lends its currency to central bank B and takes central bank B’s currency as collateral (e.g., the Fed lends dollars to the Bank of Japan and takes yen as collateral). A foreign currency (FX) repo is when central bank A lends its currency to central bank B and accepts some “hard” collateral (usually sovereign debt denominated in central bank A’s currency; e.g., the Fed lending dollars to the Brazilian central bank and accepting US Treasury securities as collateral).

The most well-known FX repo facility is the Fed’s FIMA Repo facility, which lends dollars to foreign monetary authorities, taking Treasury securities as collateral. It is, like the Fed’s swap lines, staffed and operated by the Federal Reserve Bank of New York, and has had some recent activity. Somewhat famously, the Swiss National Bank drew on FIMA to provide dollar liquidity to Credit Suisse.

EUREP: silent second

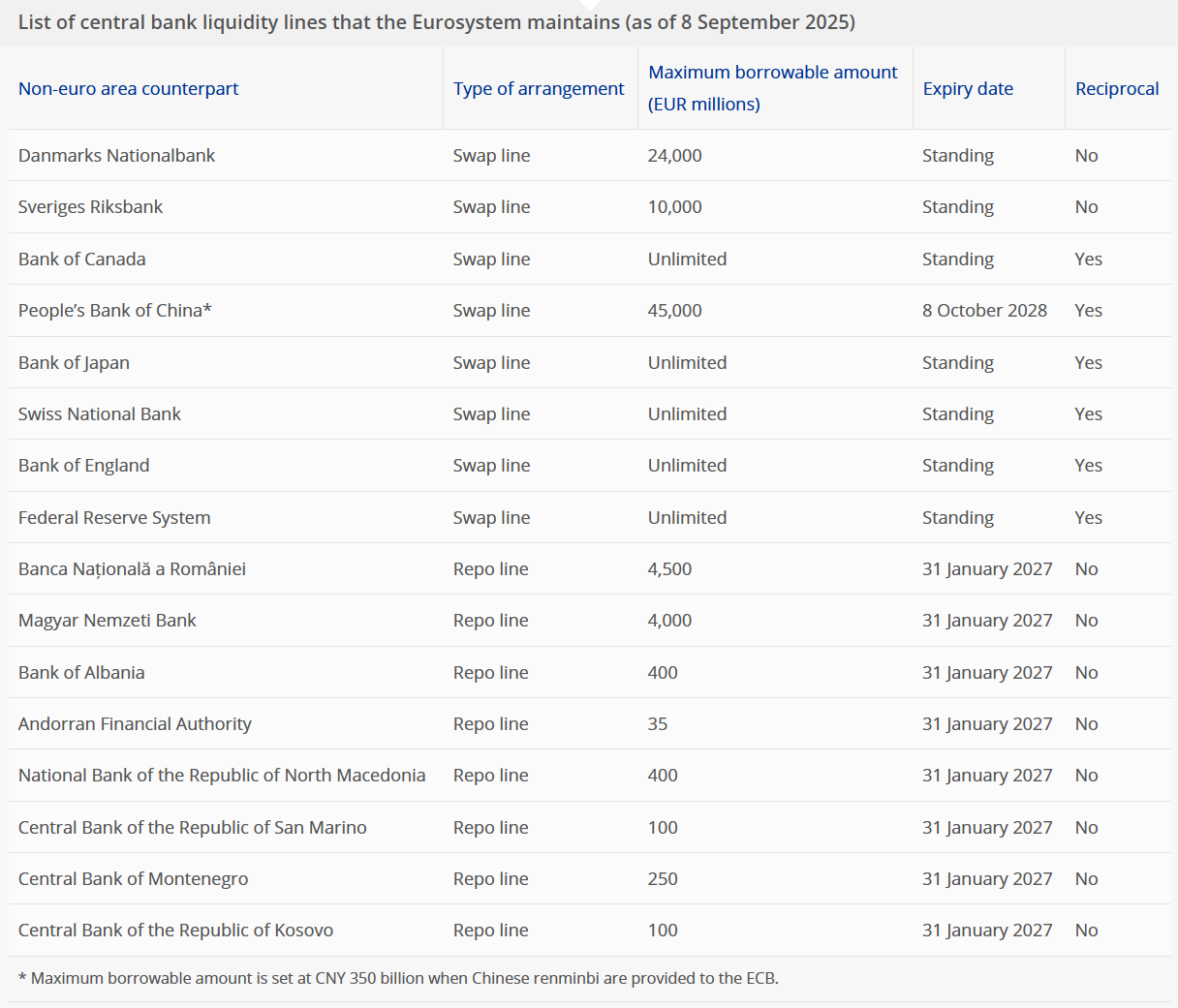

The European Central Bank (ECB) has its own version of FIMA Repo, called the Eurosystem’s repo facility for central banks (EUREP). I published a research paper on EUREP back in 2023, when I felt I was probably one of ten people outside the ECB who knew or cared about it. In contrast to the Fed, the ECB maintains three lines of liquidity defense: swap lines, bilateral repo lines, and EUREP. At least in 2023, the main recipients of the bilateral repo lines were Euro Area-adjacent (e.g., Albania, North Macedonia, etc.). EUREP’s collateral schedule was also narrower than that for the bilateral repos. Counterparts to EUREP are not disclosed by the ECB (though individual other counterparts might voluntarily disclose, as was the case then with the central banks of Kosovo and Montenegro1). For details on the facility, please see the aforementioned paper and the ECB’s website on its liquidity lines.

Source: ECB

Emergency liquidity for new geopolitics?

In a story covered by Central Banking, the ECB announced on Saturday (Feb. 14) that it would “enhance” EUREP. Here’s the meat of the language of that press release (with my emphasis):

The Governing Council of the European Central Bank (ECB) has decided to enhance the Eurosystem repo facility for central banks (EUREP) to make it more flexible and effective in supporting the smooth transmission of euro area monetary policy.

Under EUREP, the Eurosystem provides backstop euro liquidity to non-euro area central banks against high-quality euro-denominated collateral, with appropriate risk mitigants. The updated framework introduces standing access, in principle, for all central banks, unless excluded on the grounds of, in particular, money laundering, terrorist financing or international sanctions. The framework will enable central banks in jurisdictions outside the euro area to address risks of euro liquidity shortages swiftly. These changes aim to make the facility more flexible, broader in terms of its geographical reach and more relevant for global holders of euro securities.

Since EUREP was first introduced in 2020, the world economy has undergone profound structural shifts related to geopolitics and changes in the international financial system. These shifts have altered the dynamics of global trade and financial integration and suggest that the macroeconomic and financial environment will remain uncertain and potentially more volatile. More frequent financial disruptions and possible knock-on effects on euro area financial markets have the potential to hamper the smooth transmission of monetary policy.

Liquidity lines such as EUREP help support the smooth transmission of monetary policy in the euro area. They help mitigate potential negative spillover effects on euro area financial market conditions by addressing risks of disruptions in euro-denominated funding markets outside the euro area. In the context of greater fragmentation and uncertainty, Eurosystem liquidity facilities like EUREP will continue to ensure the timely, consistent and broad provision of backstop funding for central banks.

EUREP complements the ECB’s swap lines, which remain unchanged.

Now, it’s worth revisiting why the ECB has euro liquidity lines at all. The straightforward answer should be financial stability, which it mostly is: per the ECB, the cited motivations for maintaining central bank liquidity lines are to combat “market dysfunctions,” and to be used as monetary policy instruments. But, importantly, also because “they strengthen the role of the euro in international financial markets, thereby further enhancing the effectiveness of ECB monetary policy transmission” (my emphasis).

Look, if I were Europe, having just stared down the barrel of a potential American military invasion of European territory, I would probably be thinking that “structural shifts related to geopolitics” is a conversative way to put it. Note also the date of the press release, which overlapped with the Munich Security Conference. Indeed, this was not a coincidence. As Central Banking reported, ECB President Christine Lagarde gave a speech at the Munich Security Conference on the same day as the ECB press release, opening a roundtable titled “Chain Reaction: Navigating Geoeconomic Shifts and Dependencies.” Here are some excerpts (my emphasis, bolded):

What does this mean from the ECB’s perspective? Let me focus on one key initiative.

The ECB needs to be prepared for a more volatile environment. As industrial policy becomes more assertive, geopolitical tensions rise and supply chains are disrupted, financial market stress is likely to become more frequent.

We must avoid a situation where that stress triggers fire sales of euro-denominated securities in global funding markets, which could hamper the transmission of our monetary policy. And this means we have to give partners who want to transact in euros the confidence that euro liquidity will be available if they need it.

That is why, last week, the Governing Council decided to expand our EUREP facility – our standing facility that offers euro liquidity against high-quality collateral.

This expanded facility provides permanence: central banks outside the euro area can now rely on continuous access to liquidity in euros, not just temporary lines.

It extends scope: we move from a regional to a global perimeter. Any central bank that meets basic criteria can request access, with flexibility on usage.

And it ensures agility: access is granted by default unless there is a reason to restrict it, speeding up the provision of liquidity.

This facility also reinforces the role of the euro. The availability of a lender of last resort for central banks worldwide boosts confidence to invest, borrow and trade in euros, knowing that access will be there during market disruptions.

In a world where supply chain dependencies have become security vulnerabilities, Europe must be a source of stability – for ourselves and for our partners.

That, too, is part of European security. And that is how the ECB plays its part.

So, yeah, this is basically about geopolitics and the international role of the euro, which, fair enough—I’d be thinking the same thing. Jean Monet famously quipped that “Europe will be forged in crises, and will be the sum of the solutions adopted for those crises.” That line has aged well, and seems a fair description for major European policy initiatives. EUREP expansion may be one of them, but in service of a larger goal: expanding the international use of the euro.

Lover’s quarrel?

One might question whether the European reaction to the latest round of American policy is an overreaction, particularly given Sec. Rubio’s recent Munich speech. But again, the US implicitly (explicitly?) threatened to invade Europe to take physical territory, so it seems reasonable for Brussels to aim for more strategic autonomy on the margin. But this is also too simple a story: recall that Europe’s famous Anti-Coercion Instrument was not borne of conflict with China, but rather with America, years ago. Remember INSTEX, a (not effective) scheme to avoid sanctions? Also America, not China or Russia. This story predates the current American administration.

This is not to say that America is Europe’s main challenge—clearly far from it. And, as Sec. Rubio said, America’s “destiny is and will always be intertwined with” Europe’s. Trans-Atlanticism isn’t dead. But I mean, it isn’t in rude health either, and I don’t think we should be shocked by this showing up in the land of central banking policy-cum-diplomacy.

Will it work?

So, can Europe manage to create a compelling alternative to the dollar as an international reserve currency? Will this EUREP change do the trick? These are two distinct questions.

On the first, yes—to some degree it already has. The euro has safely been the second reserve currency for some time.

On the second, no, at least not in isolation. Pulling from an earlier piece from this site, when I was writing about the provision of swap lines by China to support renminbi internationalization:

Imagine you’re on a used car lot looking to purchase a car. As you walk past a sedan, a salesperson approaches you and says she can offer you an insurance deal on that specific car because she has a special deal with the manufacturer. Do you buy the car? I don’t know. It depends. All else equal, the provision of comparatively cheap insurance with broad coverage would, on the margin, make you more likely to buy the sedan. But not all else is equal: you’d have to want the car in the first place. Swaps lines are somewhat similar. They provide insurance against a liquidity shortage, making it easier and safer to transact in the currency and hold assets denominated in it. But again, you’d have to want to use that currency in the first place. Using the provision of insurance to enhance the desirability of the product is to put the cart in front of the horse.

Backstop liquidity provision—essentially insurance—is a necessary but far from sufficient condition to “internationalize” a currency (whatever that means to you, which seems to be in the eye of the beholder, to some degree). The lack of a generous euro liquidity safety net is not the binding constraint on the euro’s international use.

It’s the lack of more euro-denominated safe assets. Carlos Cuerpo, a Spanish minister, identified this head-on just days ago in an excellent FT Alphaville piece appropriately titled, Europe’s best bet for financial sovereignty is a true safe asset. Agreed! He’s put it better than I can, so I encourage you to read the article (FTAV is free to read). But the upshot is that the world needs safe assets; the US has manufactured them to an unparalleled degree; but there is no reason—aside from political ones—that Europe can’t expand the quantity of euro-denominated safe assets in the world.

In that case, maybe the new and improved EUREP will get some use after all.

Geopolitics matters

I think the main upshot here is less about the specifics of EUREP (although I’m so here for that) and more about the big-picture trendlines. As Bloomberg’s Joe Weisenthal and Tracy Alloway put it on a recent podcast episode (I’m paraphrasing), “we now talk about the Munich Security Conference as a macroeconomic event.” At this point, I think this realization is old(-ish) news, but that even a trans-Atlantic rift is starting to shape European central banking policy is perhaps a surprise in magnitude to some.

“We’re so back.” — geopolitics