Reading List No. 2

a discursive-ish list of things

This is the second reading list, since the first appeared to get good feedback. As usual, I will try to provide some non-gated content, but no promises. Coffee1 and newspaper time.

The Emergence of Tokenized Investment Funds and Their Use Cases. Pablo Azar, Francesca Carapella, JP Perez-Sangimino, Nathan Swem, and Alexandros P. Vardoulakis. Federal Reserve Bank of New York.

One way to think about tokenization is that it’s sort of back to the future with financial assets: the original form of tokenized claim was cash bills and tradable bills of exchange. Now we have tokenized digital assets. Stablecoins have been the first, but they have confounded many of us, since they don’t have (legal) yield. Tokenizing 2a-7 money market funds, though, now that makes some sense. It’s happening! And as the authors point out, it’s not necessarily the payment rails that are revolutionary, but rather the 24/7 trading window. Being able to post and move collateral 24/7 instantaneously is an interesting proposition.

Financial Bubbles Happen Less Often Than You Think. William Goetzmann. Wall Street Journal.

Bill Goetzmann is one of the most accomplished financial historians around, and just so happens to teach at the Yale School of Management. This is an excellent piece about the psychology of crowds, and a refreshing reminder about loss aversion bias. A nice line from the article that sums up the idea:

Since 1887, there have been just four cases where the Dow Jones Industrial Average has dropped by more than 10% in a single day—and two of those were during the big crash of 1929 . . . one of the biggest mistakes an investor can make is to rely on a handful of colorful historical episodes and ignore the long intervals in between: the sequence of quiet gains that stock markets have made over the decades and centuries they have existed.

If that didn’t hook you, perhaps the following will: he discusses the great Mississippi Company bubble of 1719–1720 in what was then French Louisiana. Incredible story, highly recommend.

Argentina Gets a Bailout, Brazil Gets the Stick. What Unites Them. Karthik Sankaran. Barron’s.

Karthik Sankaran is one of my favorite macroeconomic commentators and he has a Substack, The Home-Groan Globalist, which you should check out:

I think of this piece as the analytical pairing to my mostly descriptive recent note on the background of the Argentina aid package, here:

Karthik makes the point that Argentina is the yin to Brazil’s yang in America’s treatment of South American economies, both subject to what is little more than geoeconomic statecraft. He makes another interesting analogy: to ECB treatment of Eurozone countries during the Eurozone Crisis.

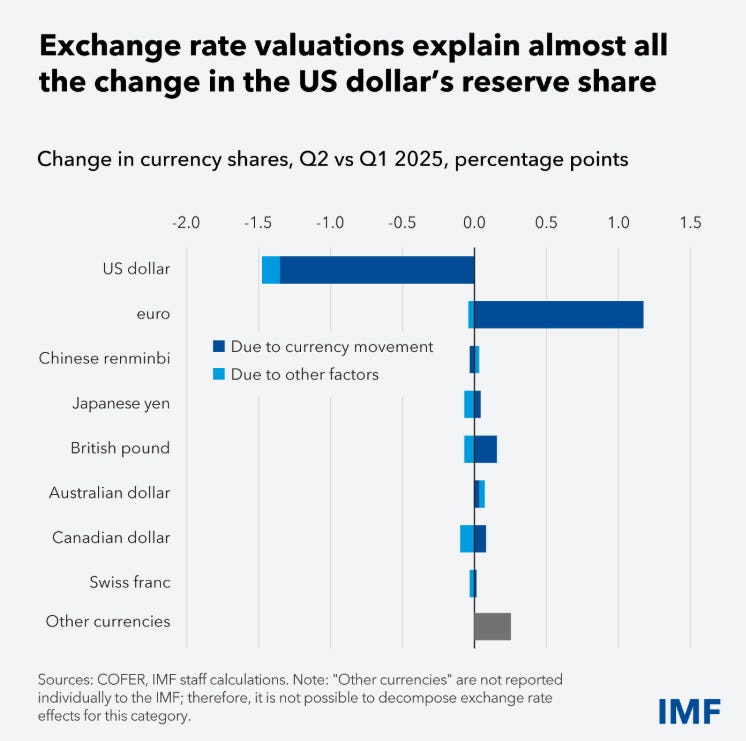

Dollar’s Share of Reserves Held Steady in Second Quarter When Adjusted for FX Moves. Glen Kwende, Erin Nephew, and Carlos Sánchez-Muñoz. IMF.

For those in the field, this has been a huge topic of conversation, and to some degree, controversy. The IMF maintains COFER data, which provides aggregated data on the currency composition of reserves (it literally stands for Currency Composition of Foreign Exchange Reserves). If you looked at the data this past year, it looked like the dollar share of reserves had been falling, and that wouldn’t be a crazy conclusion, given the chaos surrounding “Liberation Day,” attacks on Fed independence, massive fiscal overhang, and any number of erratic policy changes in the US. But the trouble is that, as the authors note (emphasis mine):

These shares are reported in US dollars . . . So, when exchange rates shift—even if no central bank buys or sells anything—reported shares change . . . [the depreciation of the dollar] means that even if central banks made no changes to their portfolios, the value of their non-dollar holdings—when expressed in dollars—increased, resulting in a corresponding decrease in the share of dollar holdings.

It’s so important it became the IMF’s chart of the week!

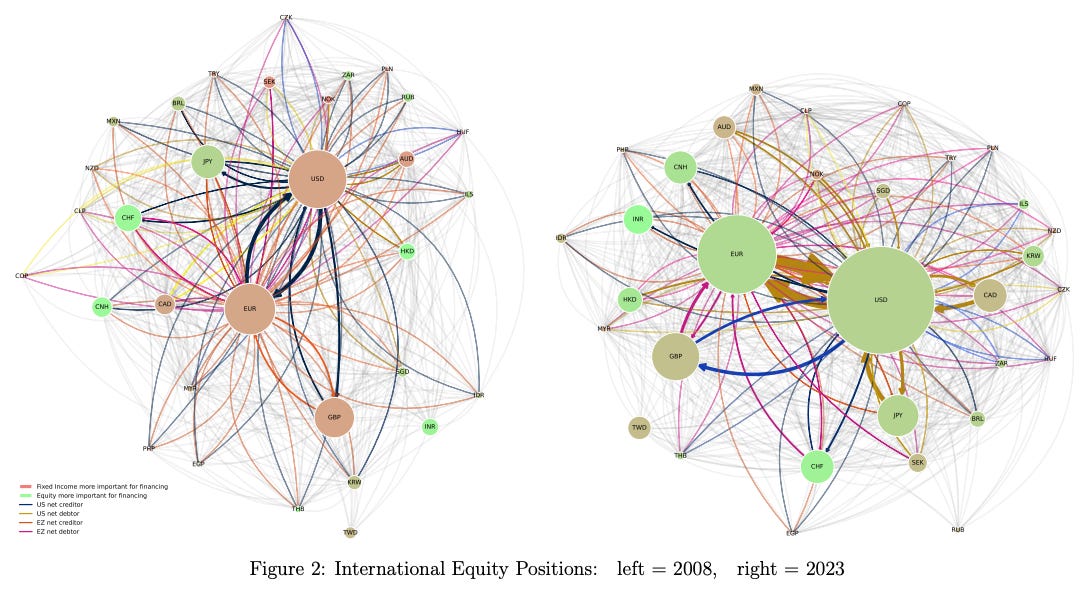

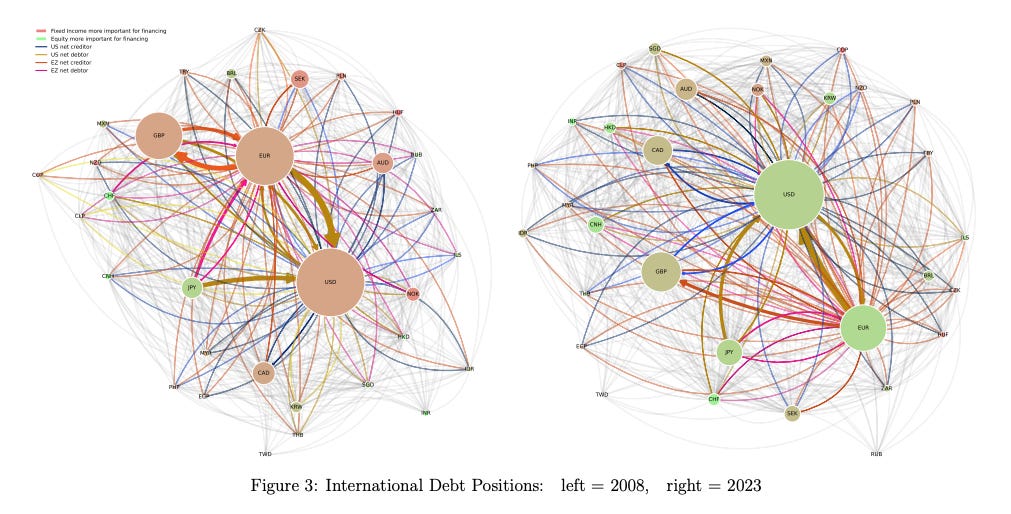

Interpreting Turbulent Episodes in International Finance. Hélène Rey and Vania Stavrakeva. Asian Monetary Policy Forum conference paper.

That capital inflows should move exchange rates and asset prices in the recipient country is seemingly obvious, but it’s one of these tricky things that’s deceptively “obvious” insofar as causal inference is notoriously difficult (because of all the endogeneity) and, as a result, so is quantification of the effect. In this paper, Rey and Stavrakeva take an instrumental variable approach (more 2SLS regressions, yay!), exploiting accounting identities about asset ownership and exchange rates, and identify a causal link.

Some of they highlights:

Equity finance is larger than debt finance in cross-border investment since 2023.

Usually, the local exchange rate appreciates on capital inflows, but there are some major and important outliers: USD (and some USD-pegged currencies), JPY, HKD, and CHF.

Foreign holdings do tend to be supportive of asset prices.

Cross-border capital markets are bigger and deeper now than in recent history.

But here’s the big one (emphasis mine):

Based on our novel daily decomposition we provide an interpretation of the striking disconnect between the USD and the standard global financial cycle that we have observed since the announcement of Trump’s tariffs. More specifically, the response to the Trump tariff announcement on April 2, 2025, marked a notable shift in global investment behavior, as the U.S. dollar depreciated sharply and foreign investors disproportionately reduced their holdings in U.S. equities and long-term government debt in favour of non-U.S. markets. This stands in stark contrast to prior crises like Covid-19 and the global financial crisis (GFC), where foreign investors typically sought safety in U.S. assets, increasing their demand for U.S. long-term government debt and decreasing demand for foreign equities in relative terms. The tariff shock represents a rare instance where global investors fled U.S. assets more than those of other countries, challenging the traditional “flight-to-safety” pattern.

We also get some very cool pictures here mapping out cross-border investments:

If I should start dropping coffee roaster recs here, let me know. I have takes. News paired with coffee, c’mon, it’s a fun idea.